Margin Reset To 15.5% Challenges Slow‑Growth Market Narrative")

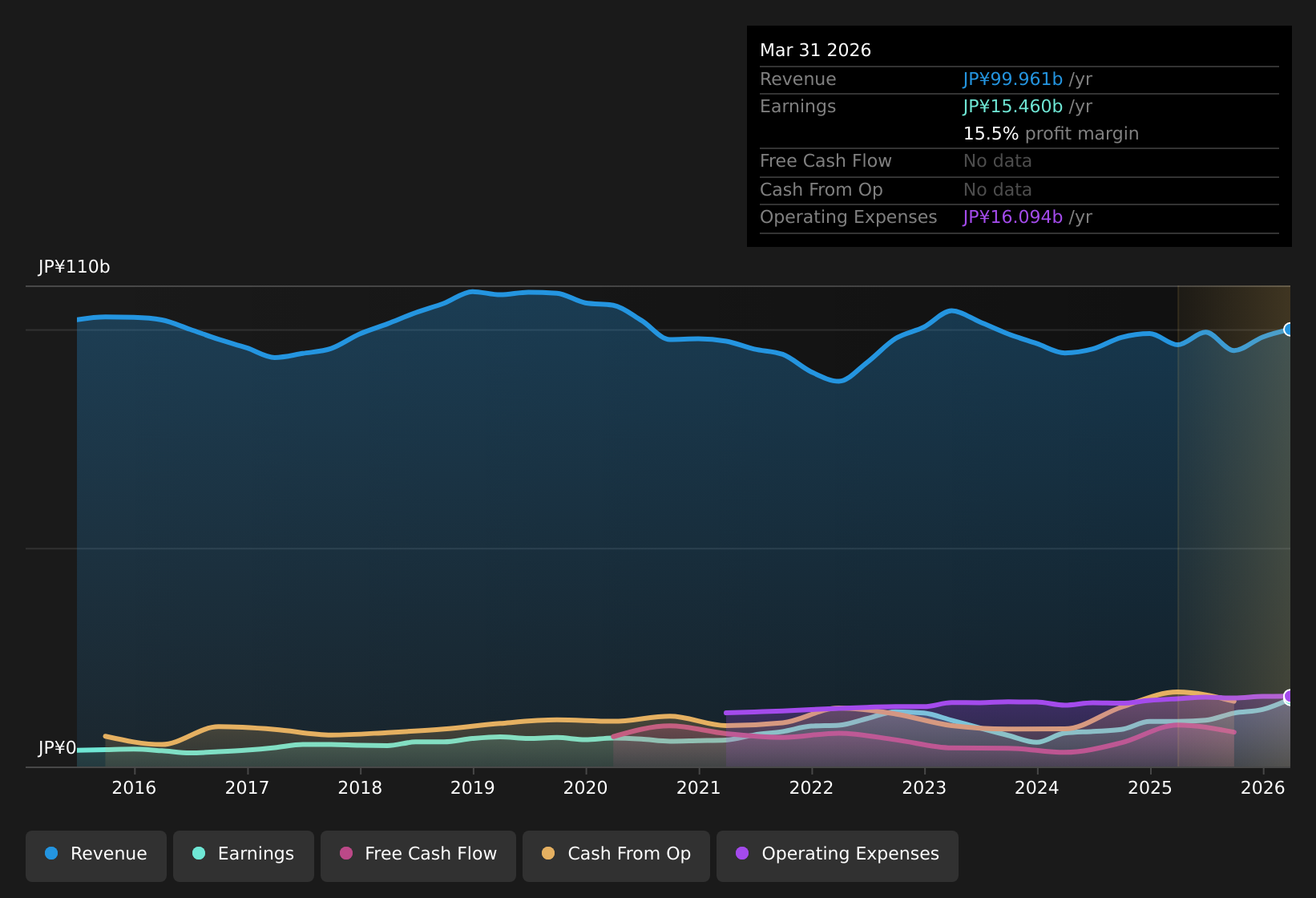

Osaka Soda (TSE:4046) has closed FY 2026 with fourth quarter revenue of about ¥26.3b and basic EPS of ¥39.17, capping a twelve month run that produced ¥99,961m in revenue and EPS of ¥123.95 on a trailing basis backed by 49.6% earnings growth over the year. Over recent periods, revenue has moved from ¥21,784m and EPS of ¥18.95 in FY 2025 Q4 to ¥26,273m and EPS of ¥39.17 in FY 2026 Q4, while trailing twelve month net income has shifted from ¥10,332m to ¥15,460m as net margin stepped up from 10.7% to 15.5%. With earnings expected to grow at about 5.7% per year from here, the key question for investors is how durable this margin profile looks after such a strong reset.

See our full analysis for Osaka Soda.

With the headline numbers on the table, the next step is to weigh them against the most common market narratives around Osaka Soda and see which stories hold up and which need a rethink.

Curious how numbers become stories that shape markets? Explore Community Narratives

TSE:4046 Earnings & Revenue History as at May 2026 15.5% net margin points to healthier profitability Trailing twelve month net income of ¥15,460m on revenue of ¥99,961m works out to a 15.5% net margin, compared with 10.7% a year earlier on ¥10,332m of net income. What stands out for a more bullish view is that this 49.6% earnings growth over the year sits on top of 8.2% annualized growth over five years, which suggests:

TSE:4046 Earnings & Revenue History as at May 2026 15.5% net margin points to healthier profitability Trailing twelve month net income of ¥15,460m on revenue of ¥99,961m works out to a 15.5% net margin, compared with 10.7% a year earlier on ¥10,332m of net income. What stands out for a more bullish view is that this 49.6% earnings growth over the year sits on top of 8.2% annualized growth over five years, which suggests:

The higher margin is not just a one quarter blip, as trailing EPS rose from ¥81.54 to ¥123.95 alongside that margin change. Stronger profitability gives Osaka Soda more room to handle a future period where earnings are forecast to grow at about 5.7% per year. Quarterly profit nearly doubles year on year In FY 2026 Q4, net income of ¥4,820m and EPS of ¥39.17 compare with FY 2025 Q4 net income of ¥2,392m and EPS of ¥18.95, so the latest quarter sits well above the year ago period on both measures. For a bullish narrative that focuses on earnings momentum, this step up in quarterly profit fits with the 49.6% trailing earnings growth, yet there are a couple of checks worth making:

Across FY 2026, revenue per quarter is tightly grouped between ¥24,284m and ¥26,273m, so the profit jump is not just about a surge in sales volumes. The steady revenue run rate alongside higher quarterly EPS suggests cost or mix effects are doing some of the work, which bullish investors may view as a sign of underlying resilience. On the back of this kind of profit progress, it is worth seeing how bullish and cautious investors frame the longer term story in more detail See what the community is saying about Osaka Soda. Valuation gap versus 7.9% revenue growth outlook The stock trades at ¥1,935 against an analyst target of ¥2,385 and a DCF fair value of ¥2,501.12, while earnings are forecast to grow about 5.7% per year and revenue about 7.9% per year compared with a 6.1% Japan market revenue reference. Critics highlight that the 5.7% earnings growth outlook is below the broader Japan market’s 10.2%, which can temper how much weight investors put on the apparent discount, yet the current data point to a more nuanced picture:

The trailing P/E of 15.4x sits below the peer average of 17x but slightly above the Japan chemicals industry at 14.3x, so the stock is not clearly expensive or cheap on a single comparison. The roughly 22.6% gap to the DCF fair value and analyst implied upside of about 23.3% coexist with that slower earnings growth profile, which is why some investors may see value while others stay focused on the growth differential versus the market. Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on Osaka Soda’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

Seen enough to sense where sentiment is heading? Use the full data and context to form your own view quickly, starting with the 4 key rewards.

See What Else Is Out There

Osaka Soda’s earnings outlook is projected to grow more slowly than the broader Japan market at 5.7% per year, which may limit the extent of any rerating investors anticipate.

If you are looking for ideas where current prices appear more compelling relative to fundamentals, it may be useful to scan the 12 high quality undervalued stocks and see which stocks stand out on your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com