Narrative")

Japan Exchange Group, Inc. recently reported higher full-year revenue and net income for the year ended March 31, 2026, lifted its year-end dividend to ¥36.00 per share from ¥19.00, and approved a share repurchase program of up to 40,000,000 shares or 3.9% of shares outstanding by October 26, 2026. Alongside stronger earnings and a planned second-quarter 2027 dividend increase to ¥30.00 per share, the new buyback framework highlights an intensified focus on returning capital to shareholders while the company also guides to operating revenue of ¥205,000 million and basic earnings per share of ¥75.39 for the year ending March 31, 2027. We will now examine how Japan Exchange Group’s strengthened dividend policy and share buyback plan shape its broader investment narrative for investors.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

What Is Japan Exchange Group’s Investment Narrative?

To own Japan Exchange Group, you need to be comfortable owning a regulated market utility whose fortunes are tied tightly to Japanese trading activity and listed-company health, rather than rapid organic expansion. The latest results and guidance reinforce that story: revenue and earnings are growing, but at a measured pace, and management is using a richer 2026 profit base to return more cash via a higher dividend and a sizeable buyback equal to 3.9% of shares. That capital return tilt is a short term support for the investment case, but it also comes alongside guidance for a lower full year 2027 dividend and only modest earnings growth, which keeps valuation risk front and center given the current premium multiples. The new buyback and dividend framework fits neatly into this tension between income support and slower expected growth.

However, one important risk could challenge this income-focused story sooner than many expect.

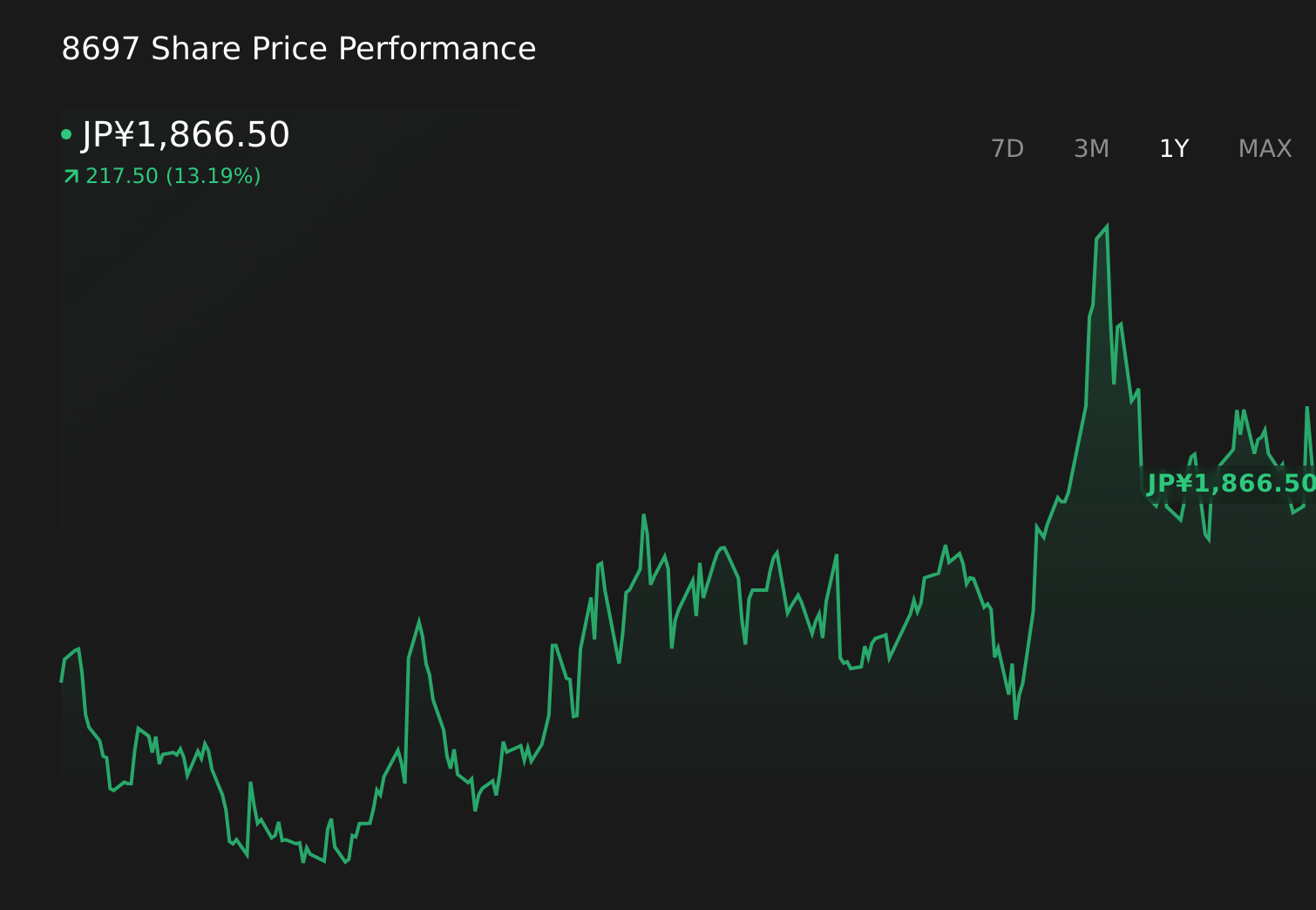

Japan Exchange Group’s shares are on the way up, but they could be overextended by 19%. Uncover the fair value now.Exploring Other Perspectives TSE:8697 1-Year Stock Price Chart With one Simply Wall St Community fair value at ¥1,562, you are seeing individual estimates sit below recent trading, while our earlier discussion of slower forecast growth and premium pricing raises questions that many will want to stress test further.

TSE:8697 1-Year Stock Price Chart With one Simply Wall St Community fair value at ¥1,562, you are seeing individual estimates sit below recent trading, while our earlier discussion of slower forecast growth and premium pricing raises questions that many will want to stress test further.

Explore another fair value estimate on Japan Exchange Group – why the stock might be worth 16% less than the current price!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com