Key points

As the largest global issuer of transition bonds, Japan is a critical test case for energy transition finance in Asia, but its financing of gas projects risks “transition washing” and normalising weak labelling practices across the region.

Analysis by the Energy Shift Institute found that the bulk of Japan’s non-sovereign transition bond proceeds funded the replacement of aged gas plants with new, high-efficiency ones. These gas-to-gas replacements often achieve only marginal annual emissions reductions due to larger capacity or higher usage, demonstrating an “efficiency paradox”.

The Climate Bonds Initiative has declined to certify subsequent Japanese GX bonds, citing the potential inclusion of controversial technologies like ammonia co-firing, which are incompatible with credible decarbonisation pathways.

Japan’s financing of gas projects in its transition bond issuances not only risks entrenching fossil fuels, but normalising such labelling practices elsewhere in Asia, warns a report by Energy Shift Institute (ESI).

Published last December, the Australia-based thinktank’s research found there is weak consensus around what counts as credible “transition” activities in Asian taxonomies which exposes investors to transition-washing risks. In addition, it showed that many gas projects barely cut lifetime emissions.

Given its outsized influence in shaping standards and credibility thresholds in the region, Japan – which accounts for 76% of global transition bond issuances – is “a critical test case for energy transition finance in Asia”, says ESI.

Under its strategic energy plan and green transformation (GX) framework, Japan recognises gas – which makes up roughly a third of its energy mix – as a fuel that can support the country’s decarbonisation goals while maintaining reliable power supply, leaving the door open for projects to be financed under its “transition” label.

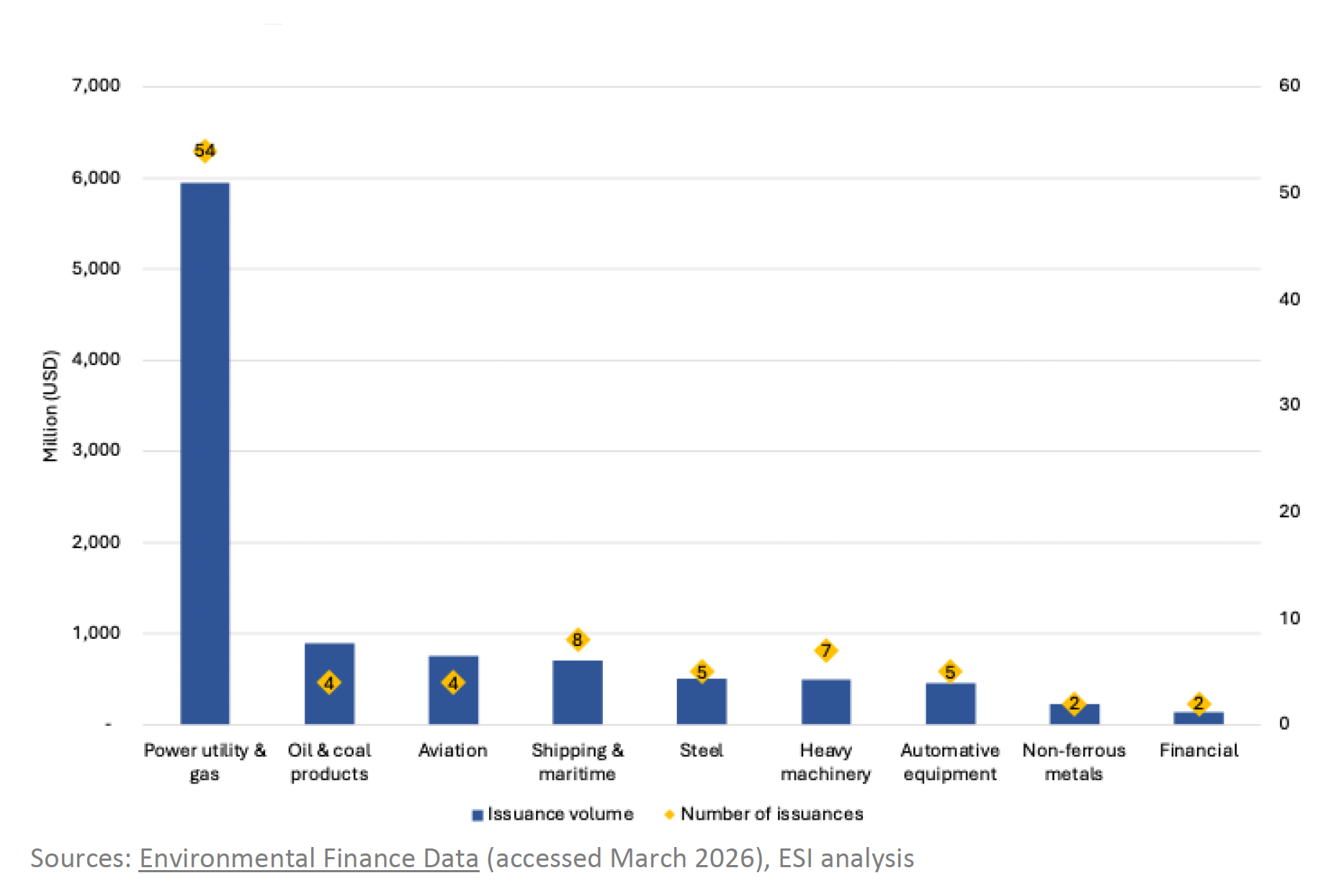

For instance, ESI’s latest analysis finds that the bulk of disclosed proceeds from Japan’s non-sovereign transition bonds issued from 2021 to 2025 went to activities across the gas value chain. At least four issuers disclosed replacing aged gas plants with new “high-efficiency” gas plants that continue to rely on liquified natural gas (LNG) as the primary fuel source.

Proceeds have also gone to research and development in ammonia and hydrogen co-firing as well as the construction of LNG infrastructure.

Japanense transition bonds by non-sovereign issuance, 2021-2025. Transition bond issuers in the power and gas sector are replacing aged gas with new gas plants. Image: ESI

Japanense transition bonds by non-sovereign issuance, 2021-2025. Transition bond issuers in the power and gas sector are replacing aged gas with new gas plants. Image: ESI

While new combined cycle gas turbines (CCGT) have a lower emissions intensity than old steam turbine plants, they do not guarantee “meaningful total emission reduction”, argues ESI.

To ensure the replacement plant “materially reduces absolute emissions”, the report states that emissions intensity improvements must not be offset by larger plant capacity or higher usage, cumulative emissions must be reduced over its operating life and there must be a time-bound plan to replace gas with a low-emission alternative or switch to renewables by 2035, in line with the International Energy Agency’s recommendations.

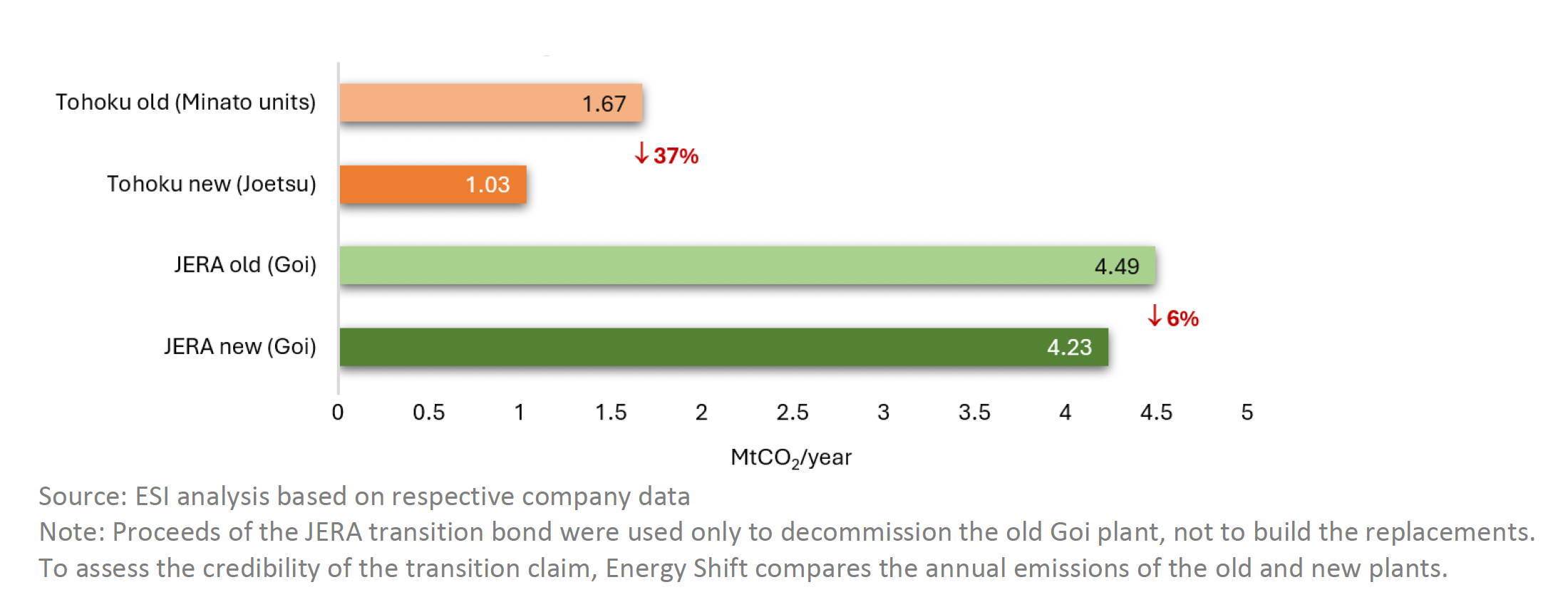

For example, ESI finds that a 2022 transition bond issued by Jera – Japan’s largest power generation firm – to replace a 1,886 megawatt (MW) gas plant with a new 2,340MW facility reaped negligible annual reductions in emissions.

Under its baseline scenario, ESI estimates that the replacement leads to a just under 6% reduction in annual emissions, after taking into account the 24% larger new capacity.

“This illustrates an efficiency paradox of gas transition investments. A plant can become far more efficient while barely moving the emission needle,” state the authors.

They add that, given modern CCGT plants are typically designed to run more often as their economic viability depends on increased usage, the replacement could even lead to a rise in annual emissions.

Furthermore, as the new gas-fired asset is substantially larger than the one it replaced in a grid where the total electricity demand is relatively stable, it “risks entrenching gas as a larger share of the generation mix – potentially displacing the low-carbon capacity, such as renewables, that a credible transition would require”.

By contrast, ESI projects that Tohoku – another Japanese utility which replaced its old gas units with a smaller one through a 2023 transition bond issuance – could see its emissions drop by 38% as a result of the smaller, more efficient replacement.

But the authors add a caveat that while Tohoku’s project cuts annual emissions, it has not spelled out usage limits or a credible pathway to mitigate carbon lock-in.

“These case studies show that a project can be technologically modern, more efficient and even labelled as a part of a transition strategy, and yet still commit the energy system to decades of substantial emissions,” they write.

Tohoku’s transition-labelled gas-to-gas project is estimated to result in larger annual emissions cuts compared to its peer utility company, Jera. Image: ESI

Tohoku’s transition-labelled gas-to-gas project is estimated to result in larger annual emissions cuts compared to its peer utility company, Jera. Image: ESI

Credibility of transition bonds called into question

Earlier this year, the Japanese government obtained a second-party opinion for its climate transition bond framework under the International Capital Market Association’s newly established climate transition bond guidelines.

However, the Climate Bonds Initiative – widely regarded as the “gold standard” certification scheme for green bonds – has declined to certify subsequent GX bonds after the initial issuance in February 2024.

One of the concerns raised was the potential inclusion of controversial technologies, such as ammonia or hydrogen co-firing, which is seen as incompatible with credible transition pathways, as Japan expands the scope of eligible expenditures.

“For transition bond investors, efficiency improvements alone are not sufficient evidence of transition. What ultimately matters is whether the project delivers sustained and optimal reductions in absolute emissions, rather than improvements that exist only under specific operating assumptions,” states ESI.

“Transition bonds must be credible to deserve the label. Gas-to-gas replacements stretch that credibility when the ‘transition’ delivers marginal emission reductions and leave the overall carbon trajectory unchanged.”

This page was last updated May 6, 2026

Written by

Gabrielle See is an award-winning journalist based in Singapore who has written for Green Central Banking since 2025. She has covered the intersections of finance, geopolitics and energy transition in Asia over the past five years for regional and international publications, including CNBC, Eco-Business, Southeast Asia Globe and the Business Times.

AloJapan.com