Q4 Loss Challenges View Of Steadily Improving Margins")

TV TOKYO Holdings (TSE:9413) has wrapped up FY 2026 with fourth quarter revenue of ¥40.6 billion and a small net loss of ¥267 million, translating to basic EPS of ¥10.03, while on a trailing twelve month basis EPS stands at ¥289.28 on net income of ¥7.7 billion and revenue of ¥164.9 billion. Over the past few quarters, revenue has run between ¥39.5 billion and ¥44.3 billion per quarter, with basic EPS ranging from ¥87.98 to ¥113.15 in the first three quarters of FY 2026. This compares with EPS of ¥61.77 on revenue of ¥41.4 billion in the same quarter a year earlier and sets up a mixed picture of a steady top line alongside shifting quarterly profitability. With net margin for the trailing year at 4.7% against 3.9% a year earlier, investors are likely to focus on how the latest quarter’s loss fits into an otherwise improving profitability profile.

See our full analysis for TV TOKYO Holdings.

With the headline numbers in place, the next step is to see how this earnings profile lines up against the widely held narratives about TV TOKYO Holdings, and where those storylines might need adjusting.

Curious how numbers become stories that shape markets? Explore Community Narratives

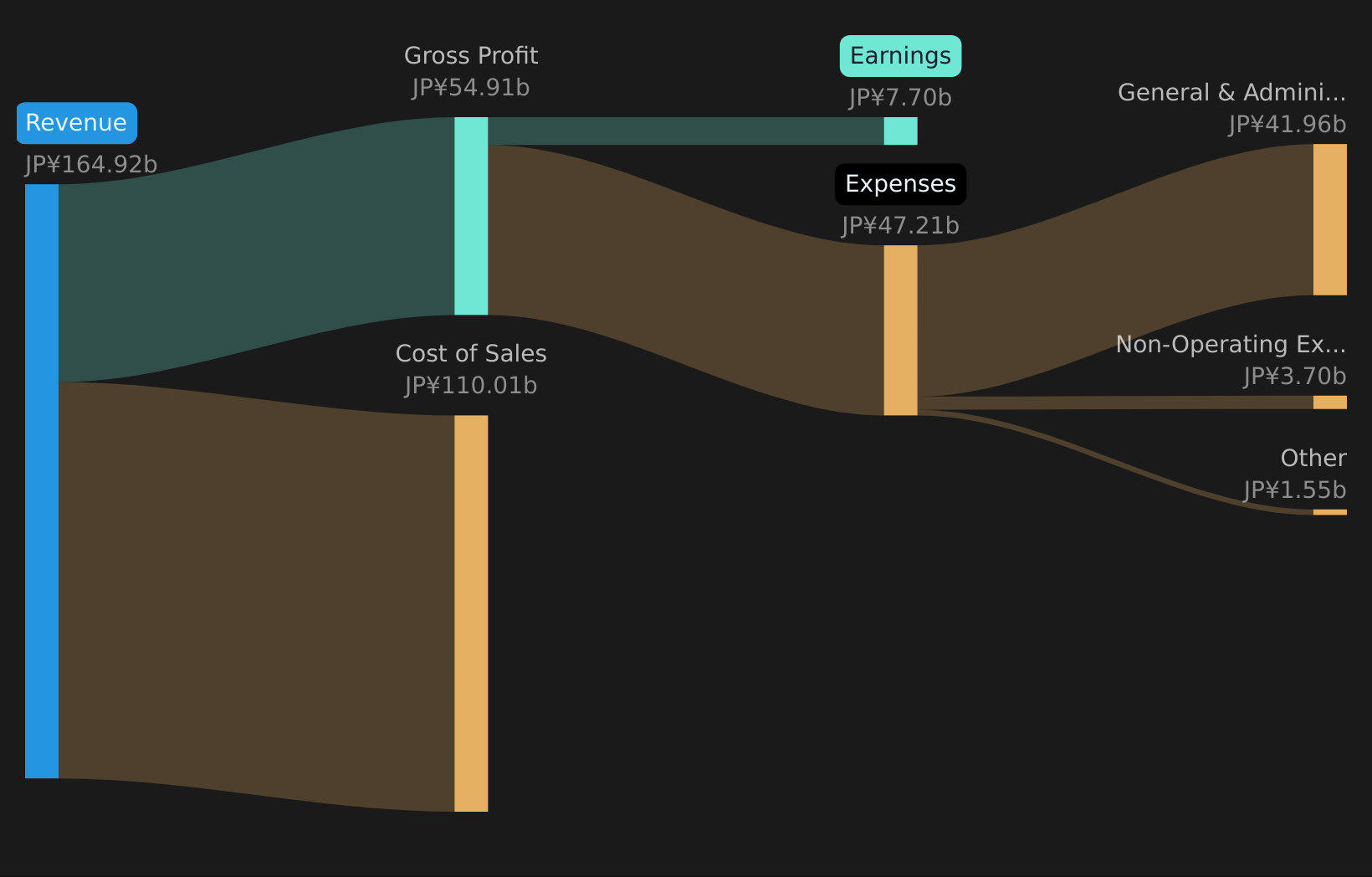

TSE:9413 Revenue & Expenses Breakdown as at May 2026 Margins Improve To 4.7% On The Year On a trailing basis, TV TOKYO Holdings earned ¥7.7 billion of net income on ¥164.9 billion of revenue, which works out to a 4.7% net margin compared with 3.9% a year earlier. What stands out for the more bullish view is that earnings grew 27.6% over the past year and 12.6% per year over five years. However, the latest quarter showed a small ¥267 million loss, so investors need to weigh the stronger full year margin against that weaker Q4 print when judging how robust the profit story really is.

TSE:9413 Revenue & Expenses Breakdown as at May 2026 Margins Improve To 4.7% On The Year On a trailing basis, TV TOKYO Holdings earned ¥7.7 billion of net income on ¥164.9 billion of revenue, which works out to a 4.7% net margin compared with 3.9% a year earlier. What stands out for the more bullish view is that earnings grew 27.6% over the past year and 12.6% per year over five years. However, the latest quarter showed a small ¥267 million loss, so investors need to weigh the stronger full year margin against that weaker Q4 print when judging how robust the profit story really is.

Supporters of the bullish angle can point to four quarters where quarterly net income ranged from ¥2.3 billion to ¥3.0 billion and basic EPS ranged from ¥87.98 to ¥113.15 before the Q4 loss. At the same time, the Q4 loss and basic EPS of ¥10.03 show that profit can be lumpy, which may temper how much confidence investors place in the trailing margin improvement. Valuation Sits Between Peers And Industry The stock trades on a trailing P/E of 13.8x compared with a peer average of 10.8x and a JP Media industry average of 15.9x, while the current share price of ¥3,995 is below the DCF fair value of ¥8,904.85. Critics with a more bearish tilt may argue that paying a higher P/E than peers only makes sense if growth matches. Yet forecasts call for earnings growth of about 3.6% per year and revenue growth of about 1.2% per year, both below the broader market forecasts shown, so the tension here is between a valuation that screens lower than the DCF fair value and slower projected growth rates.

Bears can point out that the stock trades at a premium to peers on P/E while forecast earnings growth trails the broader JP market figure of 10.2% per year. On the other hand, the large gap between the ¥3,995 share price and the ¥8,904.85 DCF fair value in the data may cause some investors to question whether the current market price fully reflects the trailing 27.6% earnings growth and higher margin. Growth Slows In Forecasts But Income Stream Helps Analysts in the dataset expect earnings to grow about 3.6% per year and revenue about 1.2% per year, while the company pays a 2.5% dividend yield based on the provided information. For investors weighing a more optimistic stance, the combination of high quality trailing earnings, five year annualized earnings growth of 12.6%, and that 2.5% dividend is balanced against the slower forecast growth. The bullish case leans on the view that a track record of profit expansion and a cash return to shareholders can still be attractive even if future growth rates are more modest than the broader JP market.

Supporters of the bullish angle may see the 27.6% trailing earnings growth and improved net margin to 4.7% as evidence that the business has been able to convert revenue into profit efficiently over the last year. At the same time, the lower forecast revenue growth of 1.2% versus the 6.1% figure cited for the broader market means any future re rating is likely to revolve around income and earnings quality rather than fast top line expansion. Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on TV TOKYO Holdings’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

If this mix of strengths and questions has you undecided, move quickly to stress test the story against the details. To examine the reward profile in more depth, take a closer look at the 5 key rewards.

See What Else Is Out There

TV TOKYO Holdings pairs modest forecast earnings and revenue growth with lumpy quarterly profits, which may leave you wanting steadier long term return potential.

If you want ideas that better balance earnings quality with growth potential, jump across to the screener containing 54 high quality undiscovered gems and quickly scan companies that might better fit your goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if TV TOKYO Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com