Valuation After Accelerated Share Buybacks")

Buyback acceleration puts Japan Securities Finance in focus

Japan Securities Finance (TSE:8511) has stepped up its share repurchase program, buying 179,300 shares in February 2026 and taking total buybacks to 1.53 million shares, or about ¥2.91b.

See our latest analysis for Japan Securities Finance.

At a share price of ¥2,251.0, Japan Securities Finance has had a 14.38% 90 day share price return and a 31.50% 1 year total shareholder return, suggesting positive momentum despite a weaker 7 day share price return.

If buybacks at Japan Securities Finance have caught your eye, it could be a good moment to broaden your search and check out 12 top founder-led companies as potential next ideas to research.

With buybacks underway and the share price already up strongly over 1 and 3 years, the key question now is simple: is Japan Securities Finance still trading at an attractive valuation, or has the market already priced in future growth?

Price-to-Earnings of 18.9x: Is it justified?

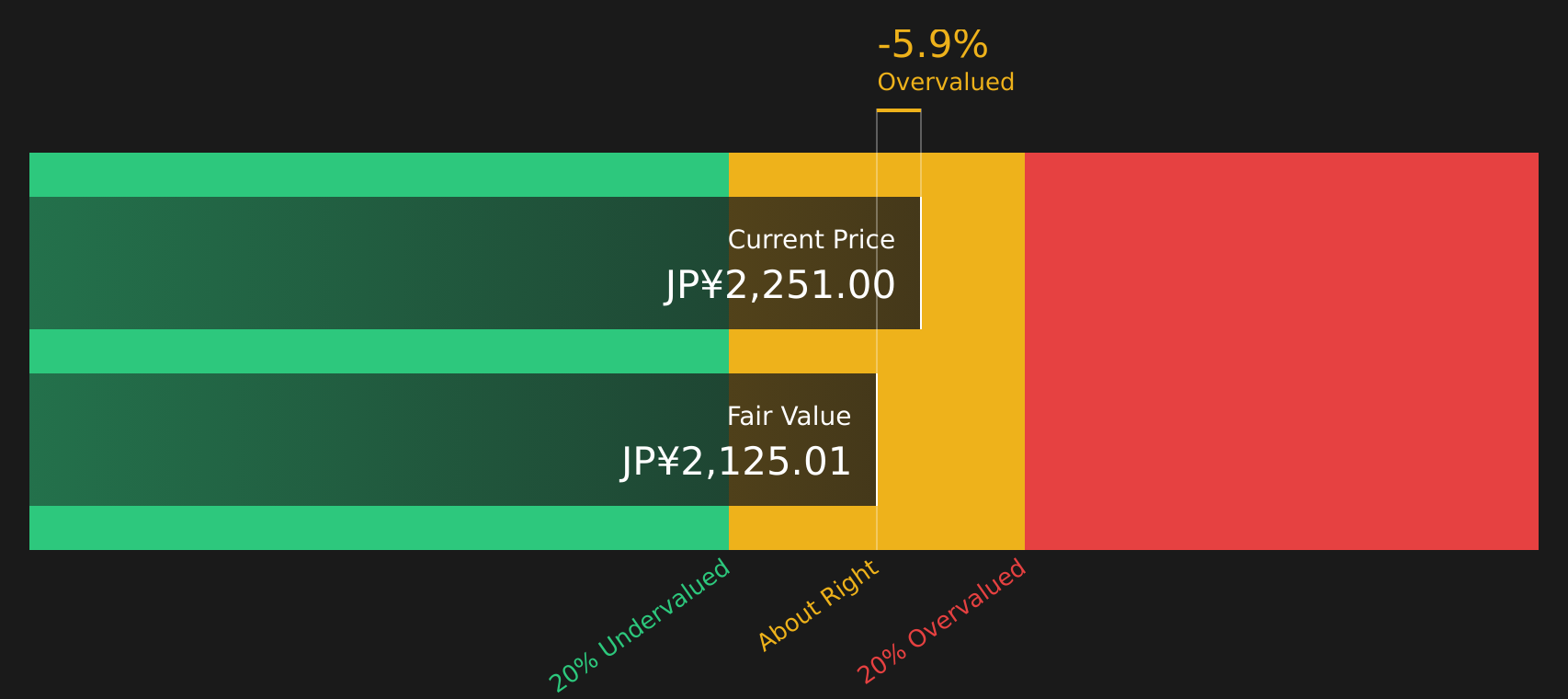

Japan Securities Finance is trading on a P/E of 18.9x, while our DCF estimate for future cash flows sits at ¥2,125.01 against the last close of ¥2,251.0. This means the market is paying a richer earnings multiple than both the peer group and the SWS DCF model suggest.

The P/E ratio compares the current share price to earnings per share, so it effectively shows how much investors are willing to pay for each unit of current earnings. For a securities finance and trust banking business such as Japan Securities Finance, this matters because earnings can be sensitive to funding costs, balance sheet structure, and market activity.

On the available data, the current multiple sits above several anchors. The company has high quality earnings and earnings have grown by 19.2% per year over the past 5 years, but the most recent year shows a 1.5% earnings decline and profit margins narrowing from 18.6% to 9.8%. At the same time, Japan Securities Finance is considered expensive relative to both the Japan Diversified Financial industry average P/E of 13.2x and a peer average of 11.1x, while the SWS DCF model points to a slightly lower cash flow based value than today’s price.

The spread is wide. A P/E of 18.9x compared with 13.2x for the industry and 11.1x for peers suggests the market is assigning a clear premium to Japan Securities Finance that may need to be supported by future execution for that premium to hold.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 18.9x (OVERVALUED)

However, you also need to weigh risks such as profit margins already narrowing and any future slowdown in securities lending or trust banking activity.

Find out about the key risks to this Japan Securities Finance narrative.

Another View: Cash Flows Point To A Similar Story

While the P/E suggests Japan Securities Finance is on the expensive side, our DCF model does not really fight that idea. With a cash flow based value of ¥2,125.01 versus the current ¥2,251.0 price, the shares look slightly overvalued on this second yardstick too.

When two very different tools, earnings and discounted cash flows, both lean in the same direction, it raises a simple question for you as an investor: what could shift in the business to change that picture?

Look into how the SWS DCF model arrives at its fair value.

8511 Discounted Cash Flow as at Mar 2026

8511 Discounted Cash Flow as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Japan Securities Finance for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 23 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If this feels like a mixed picture, do not wait around for a consensus to form. Check the details yourself, starting with 3 important warning signs.

Ready for more investment ideas?

Japan Securities Finance might be on your radar, but you do not want your portfolio relying on a single story when there are focused lists ready to explore.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com