Hokkaido Electric Power Company (TSE:9509) plans higher output and an earlier build schedule at its Ishikariwan Shinko LNG plant, moves that put its generation mix and supply reliability in sharper focus for shareholders.

See our latest analysis for Hokkaido Electric Power Company.

The Ishikariwan Shinko update comes as momentum has been firming, with a 19.06% 1 month share price return, 11.86% year to date, and a 72.38% 1 year total shareholder return suggesting investors are reassessing both growth prospects and risk.

If you are looking beyond utilities for what else is moving, our screener of 23 power grid technology and infrastructure stocks is a useful way to spot other electricity and grid related names catching attention.

With the shares up sharply over 1 year and trading at a small discount to the ¥1,340 analyst target, the key question is whether Hokkaido Electric still offers value or if the market is already pricing in future growth.

Preferred P/E of 4.4x: Is it justified?

On a P/E of 4.4x and a last close of ¥1,230.5, Hokkaido Electric trades slightly above its peer average but well below both the broader JP market and its own estimated fair ratio.

The P/E multiple compares the current share price to earnings per share. For a utility like Hokkaido Electric it reflects what investors are willing to pay for each unit of earnings given its regulated returns, capital intensity and cash flow profile.

Here, the stock is described as expensive versus its immediate peer average P/E of 4.2x. It is also framed as good value against the Asian Electric Utilities average of 17.6x and a fair P/E estimate of 9.5x, suggesting the market is pricing its earnings materially lower than the level that model implies it could move towards.

Relative to the broader JP market P/E of 15.6x, the 4.4x P/E is also much lower, which again underlines how compressed the multiple looks compared with both domestic equities and the sector wide context.

Explore the SWS fair ratio for Hokkaido Electric Power Company

Result: Price-to-Earnings of 4.4x (UNDERVALUED)

However, you still need to weigh regulatory changes or project delays at Ishikariwan Shinko that could affect earnings, cash flows, and how reliable that P/E looks.

Find out about the key risks to this Hokkaido Electric Power Company narrative.

Another view: DCF points the other way

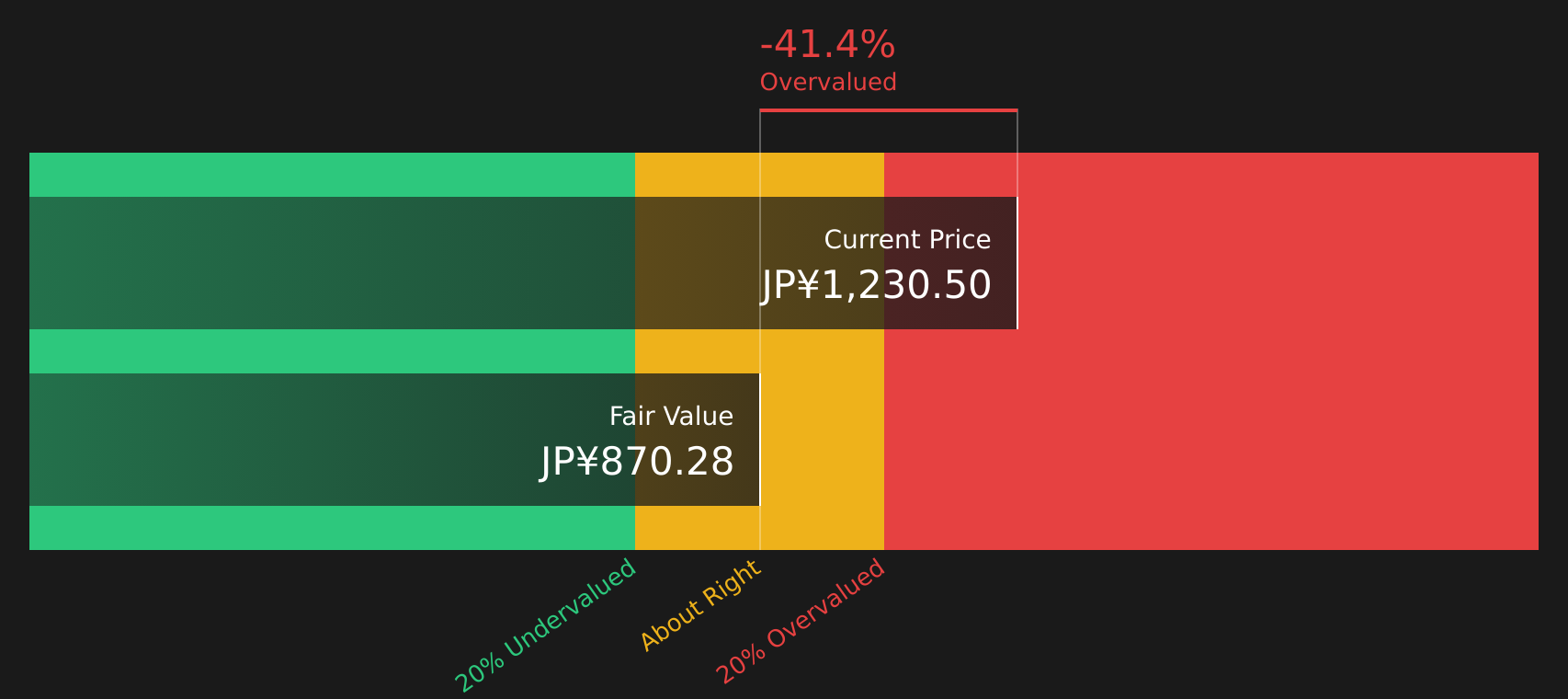

While the 4.4x P/E suggests room to move closer to the 9.5x fair ratio, our DCF model is more conservative. On that approach, Hokkaido Electric at ¥1,230.5 is trading above an estimated future cash flow value of ¥870.28, which implies limited upside and some valuation risk. Which signal do you put more weight on: earnings today or cash flows projected ahead?

Look into how the SWS DCF model arrives at its fair value.

9509 Discounted Cash Flow as at Mar 2026

9509 Discounted Cash Flow as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hokkaido Electric Power Company for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 20 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Feeling torn between the low P/E signal and the more cautious DCF view? Consider reviewing the full picture yourself, including 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If this update on Hokkaido Electric has sharpened your thinking, do not stop here. Broaden your watchlist with a few targeted idea lists before you move on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hokkaido Electric Power Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com