Valuation Check After New ¥5,000 Million Share Buyback Authorization")

What Okinawa Cellular Telephone’s buyback announcement means for shareholders

Okinawa Cellular Telephone (TSE:9436) has authorized a share repurchase program of up to 1,700,000 shares, or 1.85% of its issued share capital, capped at ¥5,000 million through April 16, 2027.

The Board describes the buyback as a way to return profits to shareholders and improve capital efficiency. This puts the focus on how reduced share count and capital allocation priorities might affect your long term exposure to the stock.

See our latest analysis for Okinawa Cellular Telephone.

The buyback news comes as the share price sits at ¥3,350.0, with a 1-day share price return of 2.45% and year to date share price return of 16.48%. The 1-year total shareholder return of 49.72% and 5-year total shareholder return of 205.30% point to strong momentum that has built over several years rather than just a short term move.

If this kind of long term compounding interests you, it may be worth widening your search and checking out our screener of 13 top founder-led companies

With a fresh buyback plan, a ¥3,350 share price and some premium to certain valuation estimates, the real question is whether Okinawa Cellular still trades below its intrinsic value or if the market already prices in future growth.

Most Popular Narrative: 2.7% Overvalued

According to AstrisCorporateAdvisory, the current share price of ¥3,350 sits modestly above a narrative fair value of ¥3,260.9, which frames the new buyback against expectations for steady but not rapid expansion.

Strong progress towards full-year forecast, FY3/26 Q1-3 sales rose +3.1% YoY to ¥64.36bn and OP increased +4.5% YoY to ¥14.35bn, as the company’s focus on improving mobile customer LTV (Lifetime Value) started showing results, with churn declining YoY for the first time in 9 quarters. Additionally, the impact from service price revisions and inter-brand migration improvement led to total mobile revenue rising +6.1% YoY.

Read the complete narrative.

Curious what sits behind a fair value that is only slightly below today’s price. The narrative leans on measured revenue growth, expanding operating profit and a margin profile that assumes Okinawa Cellular can keep extracting more value from each mobile customer without relying on aggressive top line jumps. Want to see which long term profit and cash flow assumptions support that view.

Result: Fair Value of ¥3,260.9 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, investors still need to watch for pressure on mobile competition and any shift in buyback or dividend plans that could weaken the current return profile.

Find out about the key risks to this Okinawa Cellular Telephone narrative.

Another angle on value

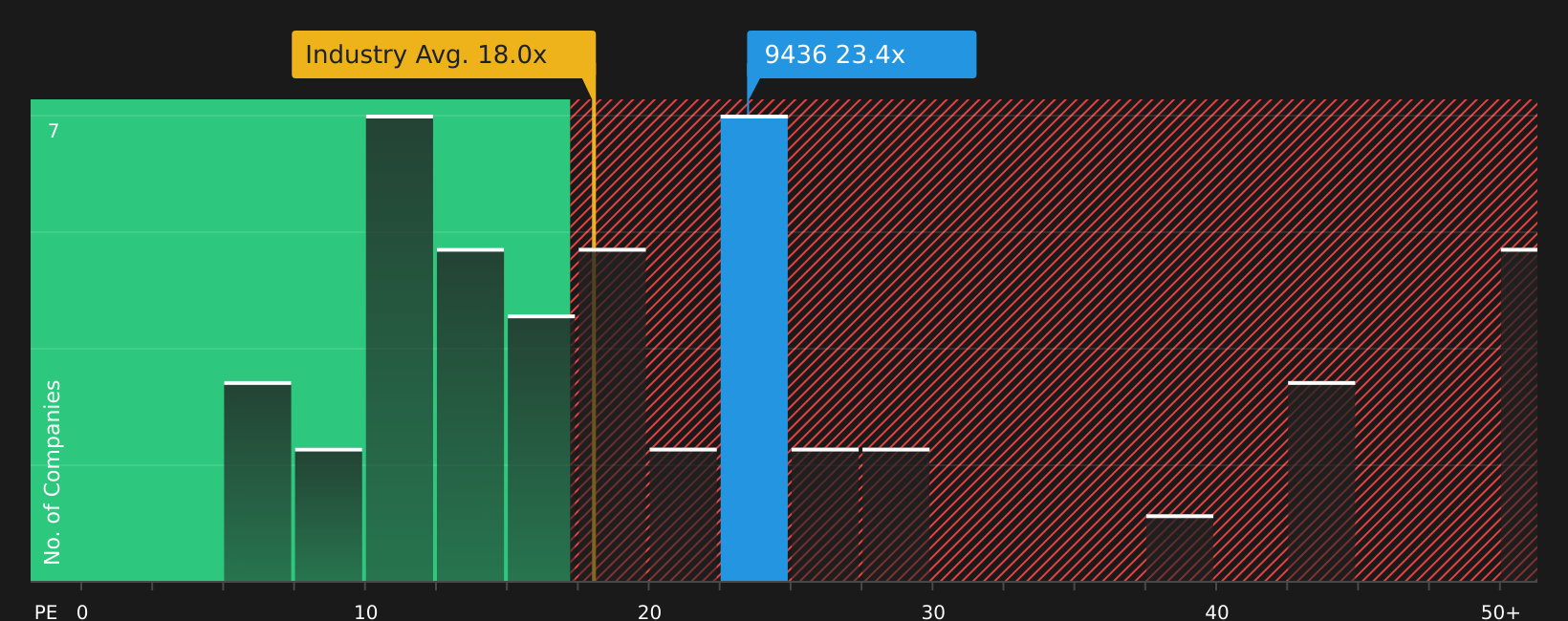

That 2.7% premium to the narrative fair value sits beside a mixed picture from simple P/E comparisons. Okinawa Cellular trades on 23.4x earnings, below a 26.2x peer average yet well above both the Asian wireless telecom industry on 18x and a fair ratio of 12.3x. For you, that split hints at either quality being rewarded or extra valuation risk if sentiment cools, so which side feels closer to the truth?

See what the numbers say about this price — find out in our valuation breakdown.

TSE:9436 P/E Ratio as at May 2026Next Steps

TSE:9436 P/E Ratio as at May 2026Next Steps

Given the mixed signals in this article, it makes sense to move quickly, review the underlying data yourself, and decide how optimistic you feel about the stock’s future rewards, starting with the 4 key rewards

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your goals even better, so broaden your search before you move on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com