Valuation After Earnings Upgrade Special Dividend And Expanded Buyback")

Kyoto Financial Group Inc (TSE:5844) has drawn investor attention after sharply raising its earnings guidance, funded by large gains on equity sales, and pairing that move with a special dividend and expanded share buyback plan.

See our latest analysis for Kyoto Financial GroupInc.

The flurry of guidance upgrades, special dividend plans and the expanded buyback has coincided with strong recent momentum, with a 30 day share price return of 15.21% and a 1 year total shareholder return of 94.36%. This suggests sentiment has shifted materially in favor of Kyoto Financial GroupInc.

If you are looking for other ideas in financials and beyond, it could be a good time to see what our screener turns up in 10 top founder-led companies and compare different types of long term compounding stories.

With gains on stock sales lifting profit guidance and a much larger stream of shareholder returns now on the table, you have to ask: is Kyoto Financial GroupInc still mispriced value, or is the market already banking on future growth?

Preferred P/E of 29.3x: Is it justified?

On Simply Wall St’s data, Kyoto Financial GroupInc trades on a P/E of 29.3x, which sits well above both its own fair P/E estimate and the wider Japanese banks sector.

The P/E ratio compares the current share price to earnings per share and is a quick way to see how much investors are paying for each unit of profit. For a bank, a higher P/E often implies the market is pricing in stronger, more durable earnings or a higher quality franchise. A lower P/E points to more muted expectations.

Here, the stock’s 29.3x P/E stands against an estimated fair P/E of 16.7x. This suggests the current price is rich relative to what the SWS fair ratio model indicates the market could move toward over time. It is also higher than the JP Banks industry average P/E of 13.2x and above the peer average of 15.1x, so the market is assigning a premium that other banks, on these metrics, do not have.

Explore the SWS fair ratio for Kyoto Financial GroupInc

Result: Price-to-Earnings of 29.3x (OVERVALUED)

However, that premium P/E and the share price sitting above the ¥3,577.5 analyst target hint at expectations that could be vulnerable if earnings or shareholder returns disappoint.

Find out about the key risks to this Kyoto Financial GroupInc narrative.

Another View: Cash Flows Point to a Different Story

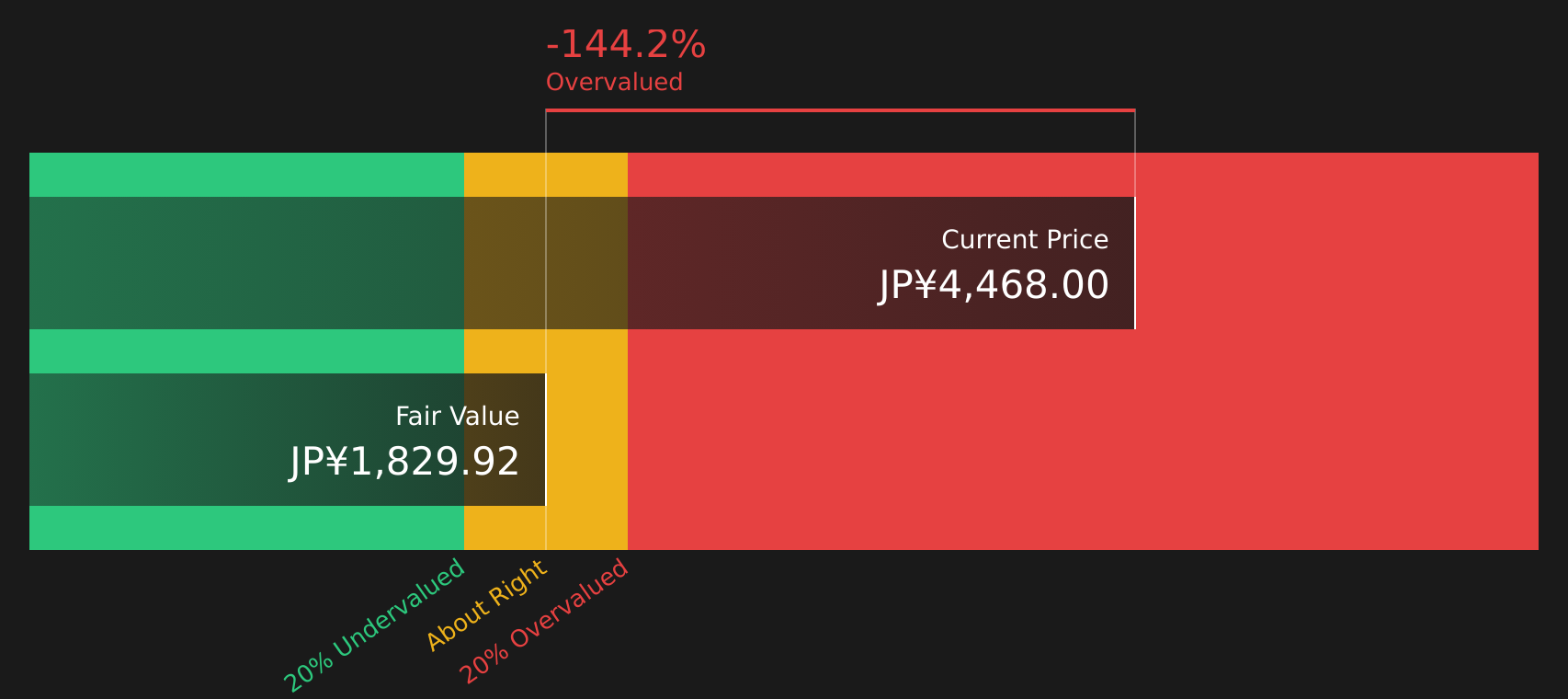

While the 29.3x P/E suggests Kyoto Financial GroupInc is expensive, our DCF model compares the current share price of ¥4,468 with an estimate of future cash flow value of ¥1,829.92. On this measure, the shares also screen as overvalued. So where could a margin of safety come from?

Look into how the SWS DCF model arrives at its fair value.

5844 Discounted Cash Flow as at Mar 2026

5844 Discounted Cash Flow as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kyoto Financial GroupInc for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 23 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed, this is the moment to look under the hood yourself and decide how you feel about the balance of risks and rewards. To frame that view with more context, take a close look at the 3 key rewards and 1 important warning sign and weigh how those factors line up with your own expectations.

Looking for more investment ideas?

If Kyoto Financial Group Inc has you thinking harder about price, quality and risk, do not stop here. Your next move could be the one that really counts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Kyoto Financial GroupInc might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com