Valuation After Ishikariwan Shinko Project Update")

Hokkaido Electric Power Company (TSE:9509) has updated its Ishikariwan Shinko Power Station plan, lifting the planned output for Unit 2 to 580,000 kW and bringing construction forward to August 2026.

See our latest analysis for Hokkaido Electric Power Company.

The updated Ishikariwan Shinko plan comes after a mixed price patch, with a 1 day share price return of 2.01% lifting the stock to ¥1,063.5, while the year to date share price return is 3.32% lower and the 1 year total shareholder return stands at 40.81%, signalling that long term holders have seen significantly stronger gains than recent traders. Looking further back, the 3 year total shareholder return of 135.91% and 5 year total shareholder return of 132.94% point to solid compounding over time, even if shorter term share price momentum has cooled recently.

If this update on Hokkaido Electric Power is on your radar, it could be a good moment to look across the wider grid transition theme with our 24 power grid technology and infrastructure stocks as a starting list of ideas.

With the Ishikariwan Shinko update, a 26% discount to the ¥1,340 analyst price target, and modest recent earnings and revenue growth, the key question is simple: is this a genuine value opportunity, or is future growth already priced in?

Preferred P/E of 3.8x: Is it justified?

On a simple earnings lens, Hokkaido Electric Power trades on a P/E of 3.8x, which sits alongside a 1 year total shareholder return of 40.8% and a last close of ¥1,063.5.

The P/E ratio compares the current share price to earnings per share, so it gives you a quick sense of how much the market is paying for each unit of profit. For an electric utility that already earns a profit and has high quality earnings flagged, this is a commonly watched yardstick.

Here, the company is on a P/E of 3.8x, which the data describes as good value versus the JP market at 14.9x, the Asian Electric Utilities average at 18x, and even its closest peer group average of 3.9x. The same framework suggests a fair P/E closer to 10.1x, which is a level the market could move towards if sentiment and fundamentals stay aligned with that regression based benchmark.

Explore the SWS fair ratio for Hokkaido Electric Power Company

Result: Price-to-Earnings of 3.8x (UNDERVALUED)

However, a 26% discount to the ¥1,340 price target and an intrinsic value premium of 22% could unwind quickly if earnings or regulation shift against expectations.

Find out about the key risks to this Hokkaido Electric Power Company narrative.

Another view from our DCF model

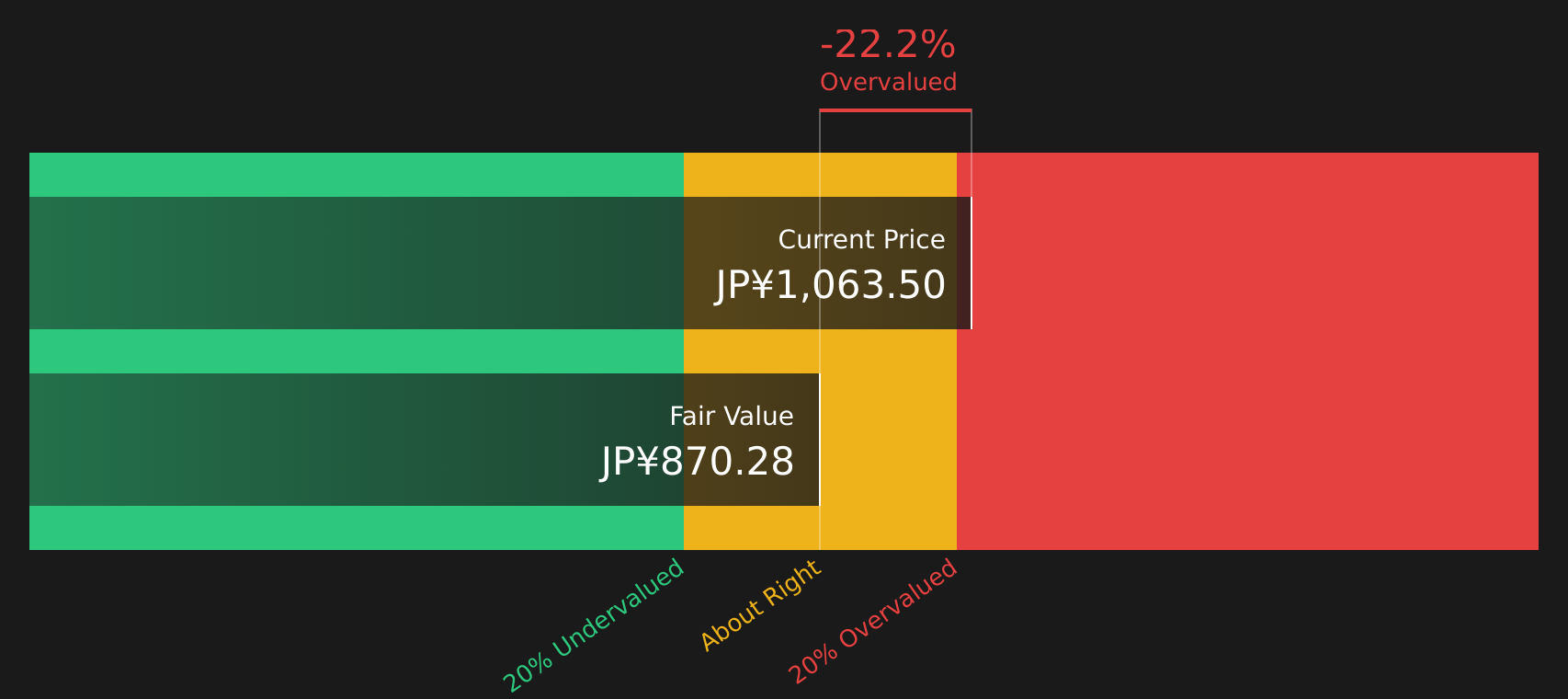

While the P/E of 3.8x looks appealing, our DCF model paints a cooler picture, with Hokkaido Electric Power trading around ¥1,063.5 versus an estimated future cash flow value of about ¥870. In simple terms, the shares look overvalued on this lens. This raises the question of which signal you trust more: the P/E ratio or the DCF model.

Look into how the SWS DCF model arrives at its fair value.

9509 Discounted Cash Flow as at Mar 2026

9509 Discounted Cash Flow as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hokkaido Electric Power Company for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 24 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Curious whether this mix of low P/E, DCF caution, risks and rewards adds up for you personally? Act while the information is fresh and weigh both sides using our breakdown of 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this analysis has sharpened your thinking, do not stop here. Widen your opportunity set now so you are not relying on a single story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hokkaido Electric Power Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com