Hokkaido Electric Power Company (TSE:9509) has released its Q3 2026 scorecard, reporting revenue of ¥205.8 billion and basic EPS of ¥22.87, alongside net income of ¥4.7 billion. The company’s revenue moved from ¥229.7 billion in Q3 2025 to ¥205.8 billion in Q3 2026, while EPS was broadly similar over that period at around ¥22.83 in Q3 2025 and ¥22.87 in Q3 2026. This sets up a quarter where the key question for investors is how efficiently that top line is translating into profit.

See our full analysis for Hokkaido Electric Power Company.

With the latest figures on the table, the next step is to see how these margins and earnings trends line up with the widely held narratives around Hokkaido Electric Power Company and where those stories might be challenged by the numbers.

Curious how numbers become stories that shape markets? Explore Community Narratives

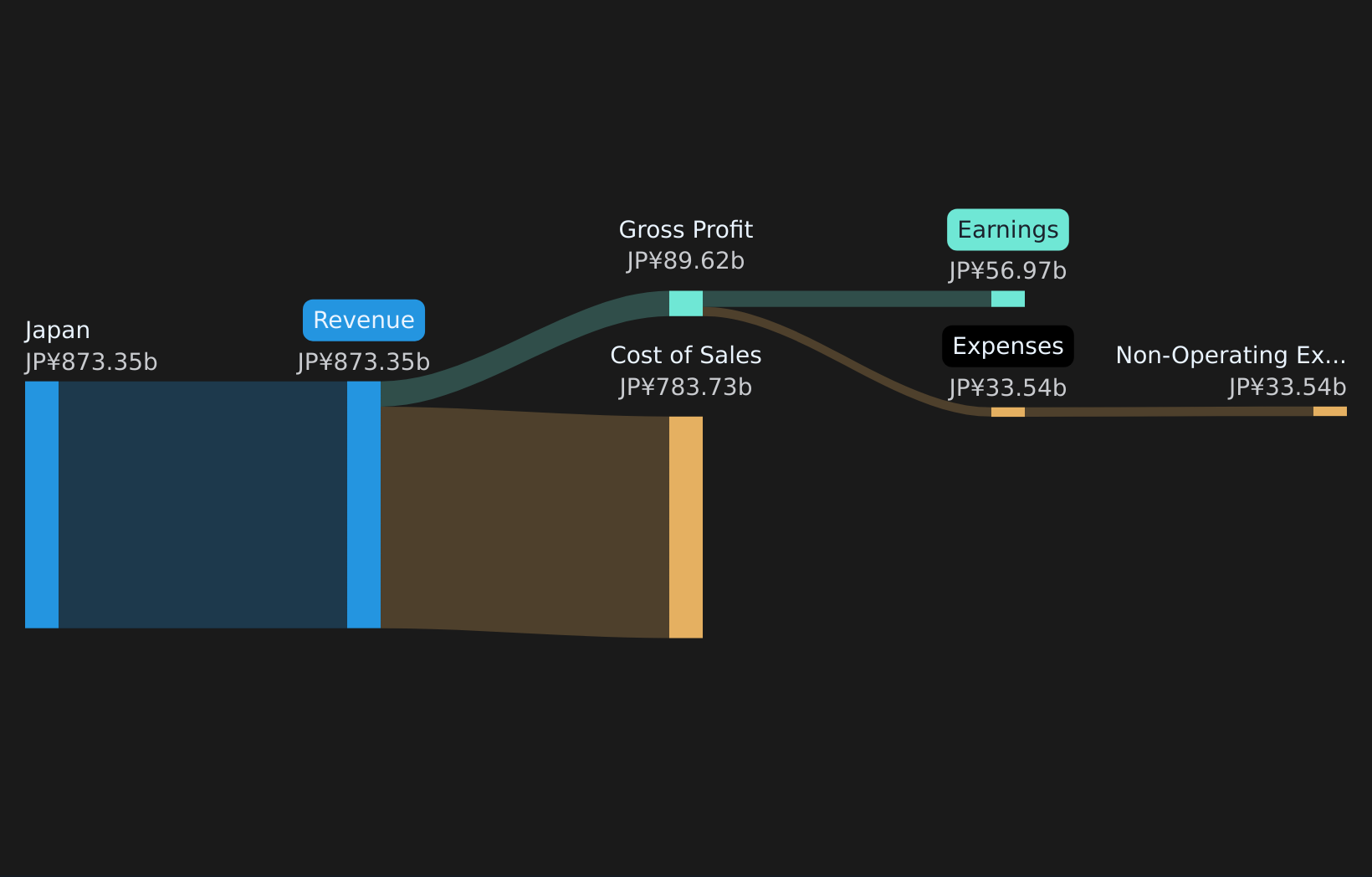

TSE:9509 Revenue & Expenses Breakdown as at Jan 2026 Margins Ease Back To 6.5% The trailing 12 month net profit margin is 6.5%, compared with 7.3% a year earlier, on revenue of ¥873.4b and net income of ¥56.97b. Bulls focusing on Hokkaido Electric Power Company as a defensive utility name run into a few numerical wrinkles here, as the modest forecast earnings growth of about 2.36% per year sits beside slower revenue growth of roughly 0.5% and a margin line that has moved from 7.3% to 6.5%. Supporters may point to the trailing 12 month EPS of ¥277.42 as evidence of earnings power, yet the step down from earlier trailing EPS levels like ¥325.62 and ¥305.90 shows that profitability per share has not been straight line. What stands out is that Q1 2026 EPS was ¥149.88 versus ¥22.87 in Q3 2026, which means short term profitability has been uneven even though the longer term view still references strong average earnings growth over the past five years. To see how these mixed margin signals fit into different long term growth stories, have a look at how various analysts lay out the full case in 📊 Read the full Hokkaido Electric Power Company Consensus Narrative.. Low 3.8x P/E And DCF Gap The shares trade on a P/E of 3.8x compared with 14.7x for the broader JP market and 16.4x for the Asian electric utilities group, while the current price of ¥1,049 sits above a DCF fair value estimate of ¥879.46. Critics who argue the stock is already pricing in the good news lean on this mix of numbers, because the low P/E ratio sits beside a DCF fair value that is below the share price and only modest forecast earnings growth of about 2.36% per year. The gap between the ¥1,049 share price and the ¥879.46 DCF fair value points to a situation where the valuation model suggests less upside than the market price implies. At the same time, the P/E sitting well below sector and market averages is consistent with a cautious stance that reflects the current 6.5% net margin and the muted revenue trend of roughly 0.5% growth. Cash Flow Strain Against Dividend The dividend yield sits at 2.86%, and the trailing analysis highlights that free cash flow does not comfortably cover this payout while debt is not well covered by operating cash flow. Bears who focus on balance sheet pressure see these cash flow gaps as central to their case, because weak coverage of both debt and dividends can limit flexibility even when trailing net income over the last 12 months is ¥56.97b. The fact that dividends are not well covered by free cash flow means the 2.86% yield is supported more by accounting profit than by cash generation, which is a key point for income focused investors to track. On top of that, the flag that operating cash flow does not comfortably cover debt adds another layer of financial risk, especially when share price volatility has already been higher than the JP market over the past three months. Next Steps

TSE:9509 Revenue & Expenses Breakdown as at Jan 2026 Margins Ease Back To 6.5% The trailing 12 month net profit margin is 6.5%, compared with 7.3% a year earlier, on revenue of ¥873.4b and net income of ¥56.97b. Bulls focusing on Hokkaido Electric Power Company as a defensive utility name run into a few numerical wrinkles here, as the modest forecast earnings growth of about 2.36% per year sits beside slower revenue growth of roughly 0.5% and a margin line that has moved from 7.3% to 6.5%. Supporters may point to the trailing 12 month EPS of ¥277.42 as evidence of earnings power, yet the step down from earlier trailing EPS levels like ¥325.62 and ¥305.90 shows that profitability per share has not been straight line. What stands out is that Q1 2026 EPS was ¥149.88 versus ¥22.87 in Q3 2026, which means short term profitability has been uneven even though the longer term view still references strong average earnings growth over the past five years. To see how these mixed margin signals fit into different long term growth stories, have a look at how various analysts lay out the full case in 📊 Read the full Hokkaido Electric Power Company Consensus Narrative.. Low 3.8x P/E And DCF Gap The shares trade on a P/E of 3.8x compared with 14.7x for the broader JP market and 16.4x for the Asian electric utilities group, while the current price of ¥1,049 sits above a DCF fair value estimate of ¥879.46. Critics who argue the stock is already pricing in the good news lean on this mix of numbers, because the low P/E ratio sits beside a DCF fair value that is below the share price and only modest forecast earnings growth of about 2.36% per year. The gap between the ¥1,049 share price and the ¥879.46 DCF fair value points to a situation where the valuation model suggests less upside than the market price implies. At the same time, the P/E sitting well below sector and market averages is consistent with a cautious stance that reflects the current 6.5% net margin and the muted revenue trend of roughly 0.5% growth. Cash Flow Strain Against Dividend The dividend yield sits at 2.86%, and the trailing analysis highlights that free cash flow does not comfortably cover this payout while debt is not well covered by operating cash flow. Bears who focus on balance sheet pressure see these cash flow gaps as central to their case, because weak coverage of both debt and dividends can limit flexibility even when trailing net income over the last 12 months is ¥56.97b. The fact that dividends are not well covered by free cash flow means the 2.86% yield is supported more by accounting profit than by cash generation, which is a key point for income focused investors to track. On top of that, the flag that operating cash flow does not comfortably cover debt adds another layer of financial risk, especially when share price volatility has already been higher than the JP market over the past three months. Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on Hokkaido Electric Power Company’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

See What Else Is Out There

Hokkaido Electric Power Company is contending with easing margins, uneven quarterly EPS, stretched cash flow coverage of its dividend, and debt that is not comfortably backed by operating cash flow.

If that mix of tight cash coverage and balance sheet pressure makes you uneasy, you may wish to shift your focus toward companies with stronger cushions and healthier funding flexibility using solid balance sheet and fundamentals stocks screener (389 results) today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hokkaido Electric Power Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com