Valuation After Leadership Reshuffle And COO Appointment")

Leadership reshuffle at Japan Exchange Group

Japan Exchange Group (TSE:8697) has outlined a broad leadership reshuffle, with long serving executive Iwanaga Moriyuki set to retire and Yokoyama Ryusuke becoming Representative Executive Officer, Group COO, from April 1, 2026.

See our latest analysis for Japan Exchange Group.

The leadership announcement comes after a strong run in the shares, with a 23.47% 1 month share price return and 39.85% 1 year total shareholder return. The 3 year total shareholder return of 128.92% suggests that momentum has been in place for some time.

If this reshuffle has you thinking about where else capital could work, it might be a good moment to broaden your search and check out 12 top founder-led companies.

With Japan Exchange Group up sharply over 1 month, 1 year and 3 years, and the shares trading at a premium to the ¥1,850 analyst target and intrinsic value estimates, is there still a buying opportunity here, or is the market already pricing in future growth?

Preferred P/E of 31.8x: Is it justified?

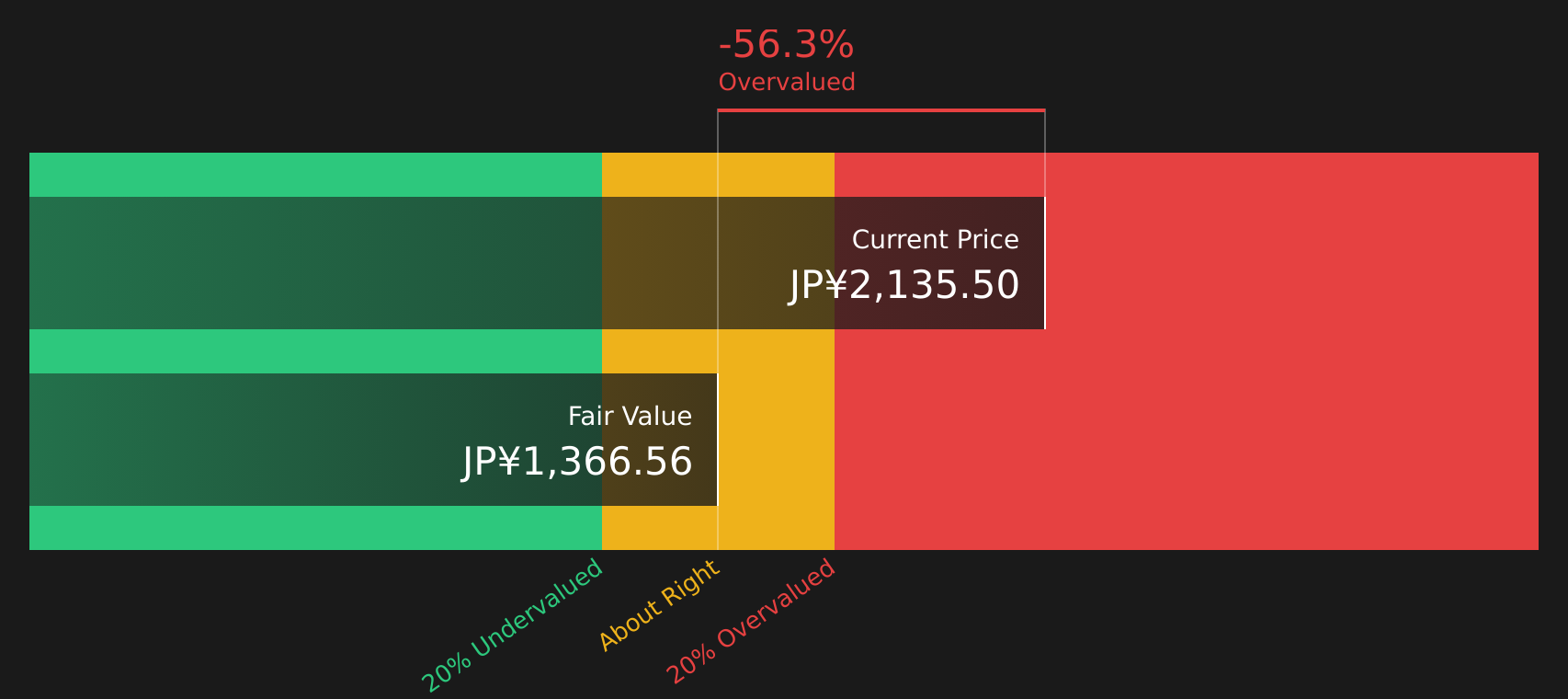

Japan Exchange Group shares last closed at ¥2,135.5, and the stock is described as expensive on a P/E of 31.8x compared with both its peers and the broader Capital Markets industry.

The P/E multiple compares the current share price with earnings per share, so a higher P/E means investors are paying more for each unit of current earnings. For an exchange operator with established profitability, this tends to reflect what the market is willing to pay for its earnings profile and future prospects.

Here, the 31.8x P/E sits well above the estimated fair P/E of 17.1x. The SWS fair ratio suggests the valuation could gravitate toward that level based on fundamentals. At the same time, earnings are forecast to grow 1.67% per year, which is slower than the wider JP market, and the stock is trading above the SWS DCF estimate of future cash flow value of ¥1,366.56. Taken together, the market appears to be assigning a premium price to Japan Exchange Group’s earnings compared with both its own fair multiple and its growth profile.

Against the JP Capital Markets industry average P/E of 14x, Japan Exchange Group’s 31.8x stands out as significantly higher, and it is also above the peer average of 18.1x. That kind of gap suggests investors are currently willing to pay a much richer multiple for this earnings stream than for typical names in the same industry.

Explore the SWS fair ratio for Japan Exchange Group

Result: Price-to-Earnings of 31.8x (OVERVALUED)

However, the premium P/E and share price sitting above the ¥1,850 target and ¥1,366.56 DCF estimate mean any disappointment on earnings or regulation could quickly challenge this optimism.

Find out about the key risks to this Japan Exchange Group narrative.

Another view on value: SWS DCF model

While the 31.8x P/E points to an expensive share price, our DCF model also flags Japan Exchange Group as overvalued, with the current ¥2,135.5 price above an estimated future cash flow value of ¥1,366.56. When both earnings and cash flow point in the same direction, how comfortable are you with paying this kind of premium?

Look into how the SWS DCF model arrives at its fair value.

8697 Discounted Cash Flow as at Feb 2026

8697 Discounted Cash Flow as at Feb 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Japan Exchange Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 20 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If this all feels finely balanced between optimism and caution, it is worth taking a closer look yourself and weighing the trade off between the concerns and the positives highlighted in our 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you are serious about putting your capital to work, do not stop at a single stock. Use the screener to spot other ideas before they move without you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com