’s Accelerated Ishikariwan Shinko Unit 2 Plan Means For Shareholders")

Hokkaido Electric Power recently increased the planned installed capacity at its Ishikariwan Shinko LNG thermal power station to about 580,000 kW and moved up the start of construction for Unit 2 from May 2027 to August 2026, reinforcing its thermal generation plans ahead of future demand needs. This acceleration of project timing and modest capacity uplift highlights how the utility is actively reshaping its generation mix to support supply reliability while addressing decarbonization pressures. Next, we’ll examine how accelerating Unit 2’s construction at Ishikariwan Shinko shapes Hokkaido Electric Power’s broader investment narrative.

Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

What Is Hokkaido Electric Power Company’s Investment Narrative?

To own Hokkaido Electric Power, you need to be comfortable with a regulated utility that is still reshaping its balance between reliability, capital intensity and decarbonization. Short term, the key catalysts remain earnings delivery against the updated FY2025/26 guidance, the recently increased dividends, and how the market continues to price a low P/E against modest growth forecasts. The Ishikariwan Shinko Unit 2 acceleration fits into this by modestly reinforcing the investment story around supply stability, but it also underscores the ongoing need for heavy capex in a business where debt is not well covered by operating cash flow and dividend cover looks tight. Given the already strong share price gains, this project tweak looks more incremental than transformational to the near term risk‑reward.

However, investors should be aware of how rising capex could strain cash generation and dividends.

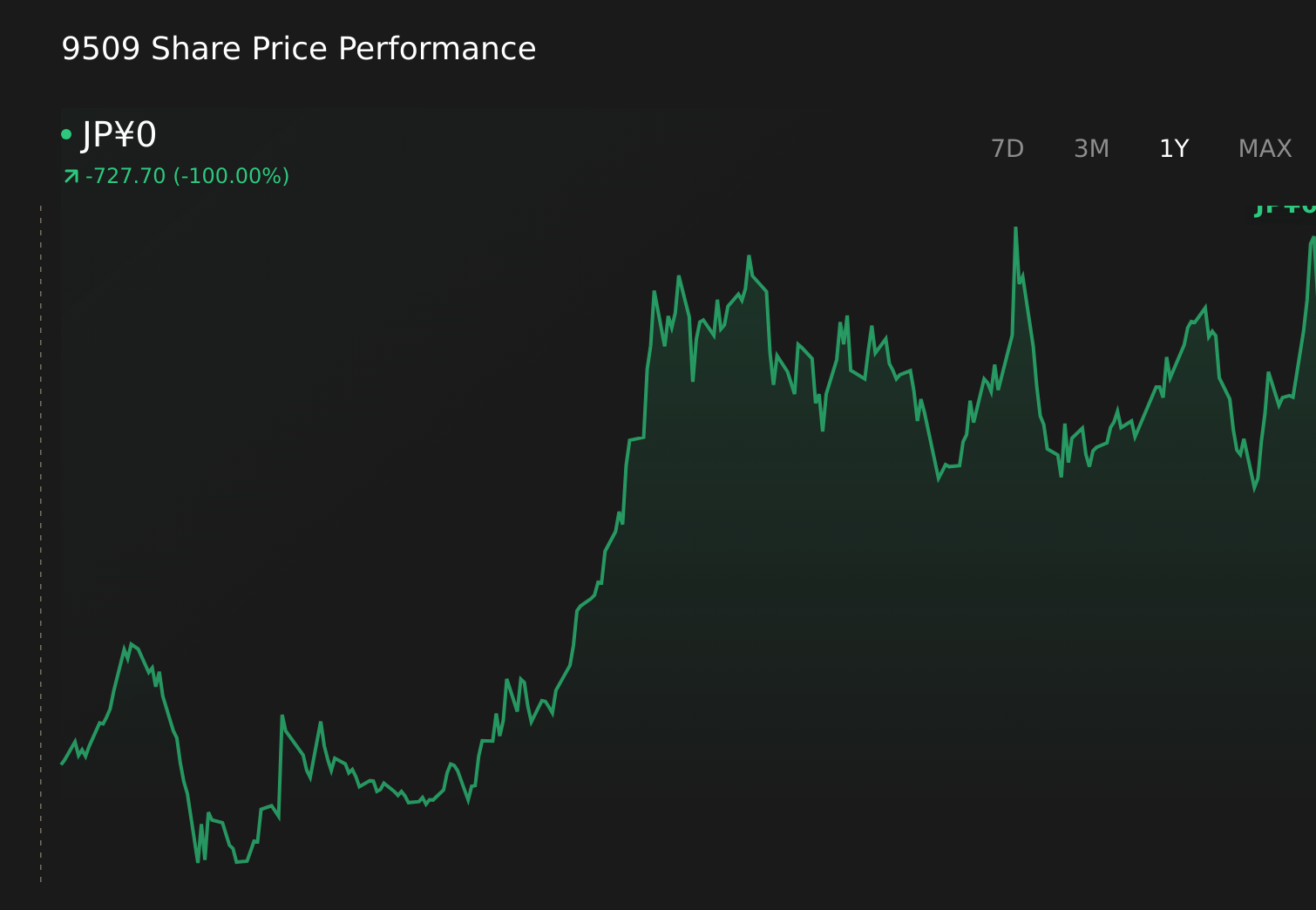

Hokkaido Electric Power Company’s shares are on the way up, but they could be overextended by 35%. Uncover the fair value now.Exploring Other Perspectives TSE:9509 1-Year Stock Price Chart The single fair value estimate from the Simply Wall St Community centers tightly around ¥909.82 per share, contrasting with recent market pricing. When you set that against capex, balance sheet and dividend pressures discussed above, it underlines how differently participants can weigh Hokkaido Electric Power’s evolving risk profile and encourages you to consider several viewpoints before forming a view.

TSE:9509 1-Year Stock Price Chart The single fair value estimate from the Simply Wall St Community centers tightly around ¥909.82 per share, contrasting with recent market pricing. When you set that against capex, balance sheet and dividend pressures discussed above, it underlines how differently participants can weigh Hokkaido Electric Power’s evolving risk profile and encourages you to consider several viewpoints before forming a view.

Explore another fair value estimate on Hokkaido Electric Power Company – why the stock might be worth as much as ¥910!

The Verdict Is Yours

Disagree with this assessment? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hokkaido Electric Power Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com