For foreign buyers looking at Japan today, the conversation has quietly shifted. The question is no longer whether Japan remains a safe and investable market — that has largely been settled — but where, within Japan, capital is working hardest now. While Tokyo continues to dominate headlines, investor behaviour tells a more nuanced story, with growing attention on secondary cities offering clearer income visibility and more balanced risk-return profiles.

Tokyo’s recovery remains real and structurally sound, supported by deep liquidity and institutional demand. However, for overseas buyers — particularly those prioritising rental stability and entry pricing — the city is no longer the only logical gateway. For Singapore-based investors, secondary cities such as Osaka and Kyoto offer strong fundamentals, where investment outcomes are often more transparent.

This shift is no longer fringe. It reflects changing demand patterns, shifting tourism flows and a maturing short-stay rental ecosystem.

Read also: Japan’s property market demands a new adaptive playbook for investors

Launched last July, Singaporeans snapped up 60% of Matro City Osaka over one weekend, at prices from $130,000 (Photo: Savills Singapore)

Short-stay demand is stronger outside Tokyo than many expect

While Tokyo’s core appeal lies in its liquidity, global visibility and long-term appreciation, these qualities come with high entry pricing and compressed yields that can make short-term cash flow strategies less compelling for investors. Osaka and Kyoto, in contrast, are more accessible price-wise and offer a diversity of asset types, from refurbished traditional housing to purpose-built short-stay developments.

In Osaka, a typical short-term rental generated a median annual revenue of about JPY4 million ($32,400) over the past year, with an 88% occupancy rate and roughly 12,000 active listings. Average annual revenue for Airbnb listings in Kyoto was even higher at around JPY5 million, with an 82% occupancy rate between late 2024 and late 2025. What matters here is not peak performance, but consistency of demand — something income-focused investors increasingly prioritise.

These figures also compete impressively with major global short-stay markets and highlight why refurbished properties in these two cities are gaining attention. One of the more under-appreciated stories in Japanese real estate — and one that international buyers are starting to price in — is the value uplift from refurbishment and conversion of existing stock for hospitality use.

Grand City Osaka B&B project (left) was launched in Singapore in November. One City Osaka (right) is part of a series of projects including Grand City, Sky City, and Metro City Osaka, by TY Properties Development, a Japanese developer, operator and manager of guesthouses. (Images: Savills Singapore)

Refurbishment is where secondary cities create an edge

Japan has a sizeable inventory of older buildings and vacant properties, especially outside central Tokyo. Investors are acquiring these assets at attractive prices, then renovating or retrofitting them into short-stay rentals, boutique hotels and serviced apartments, thereby effectively unlocking value that Tokyo’s hyper-priced new developments cannot match.

Refurbishment and hospitality conversion sharpen this advantage in three ways:

Lower acquisition costs — older buildings in regional hubs tend to trade well below Tokyo’s per sq m prices

Strong operational cash flows — as the revenue and occupancy data from Osaka and Kyoto show.

Value uplift through renovation — turning underused or depreciated stock into revenue-producing hospitality assets.

These factors generate robust risk-adjusted returns, especially for investors who are patient, operationally savvy, and focused on income rather than pure capital gains.

Read also: Apac real estate investment grew 13.7% in 2025, led by rebound in retail deals: Knight Frank

One Tea, a renovated development positioned as a B&B project offering high returns. (Image: Savills Singapore)

One Tea, a renovated development positioned as a B&B project offering high returns. (Image: Savills Singapore)

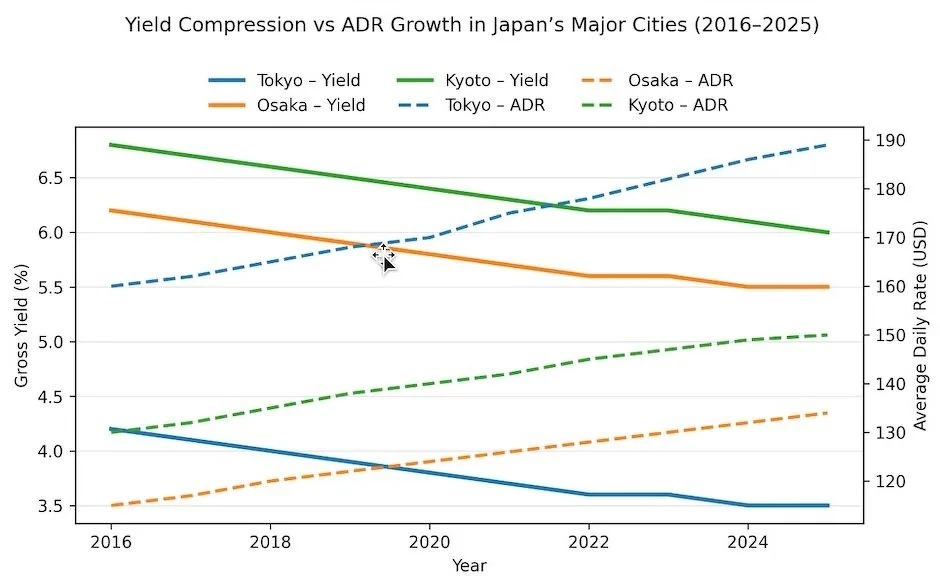

Yield compression in Tokyo, income visibility elsewhere

Tokyo’s hospitality yields have compressed steadily as pricing power pushed average daily rates (ADRs) higher, reflecting rising acquisition costs. In comparison, Osaka and Kyoto retain materially higher yields alongside consistent ADR growth, reinforcing their appeal for refurbished and hospitality-focused investments seeking stronger risk-adjusted income.

Source: Japanese brokerage estimates; short-stay rental market data

These two cities typically have lower property prices than central Tokyo. When older stock is refurbished into boutique Airbnb or hospitality assets, the cap rate achieved through renovations revenue can outperform similar investments in Tokyo’s more expensive core.

With cultural experiences being the main attraction in Kyoto, and Osaka’s robust business, entertainment and transport ecosystem, there is a steady occupant stream and diversification of guest types. For savvy investors, it’s an opportunity to shape supply rather than simply chase volume.

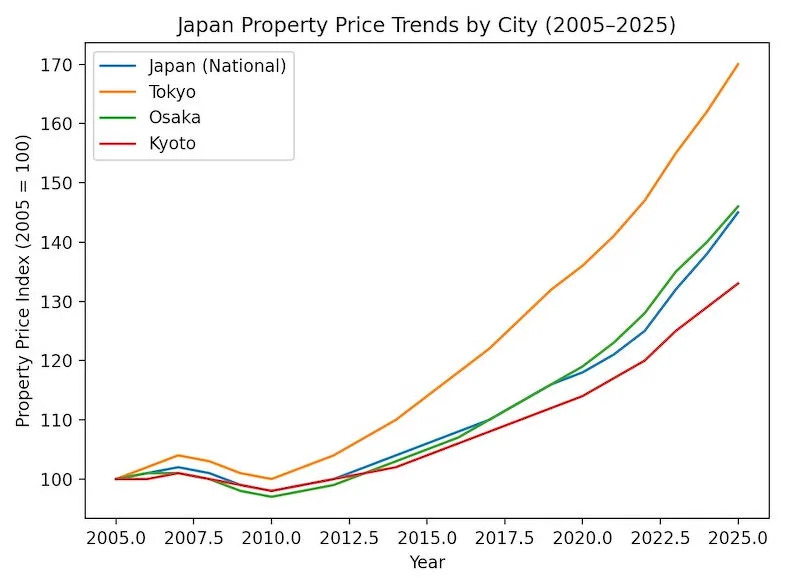

Property prices: stability matters more than speculation

Source: BIS Residential Property Price Index, Japan Ministry of Land (trend-based indices)

Source: BIS Residential Property Price Index, Japan Ministry of Land (trend-based indices)

Japan’s residential property market has moved well beyond the stagnation that followed the 1990s asset bubble, entering a phase of steady, broad-based recovery. Over the past two decades, prices across major cities have trended steadily upwards, with Tokyo leading long-term appreciation and regional centres such as Osaka and Kyoto following a more measured but consistent trajectory (see chart).

For foreign buyers, the distinction matters. Tokyo commands the highest prices and deepest liquidity, but much of that growth is already priced in. Osaka and Kyoto, by contrast, offer lower entry points within a broader recovery cycle — allowing investors to participate in both income generation and gradual capital appreciation without relying on speculative upside.

Read also: Hilton debuts Tapestry Collection by Hilton in Japan with ski lodge hotel

In practice, this has made secondary cities more attractive for refurbishment-led and hospitality-focused strategies, where income visibility and value creation matter more than headline price growth.

Currency, diversification and portfolio construction

The yen’s prolonged weakness has further sharpened interest from Asia. For Singapore-based investors, Japan offers both currency diversification and defensively priced hard assets, particularly outside Tokyo’s most competitive submarkets.

As regional portfolios become more diversified — spanning logistics, hospitality, residential and alternatives — Osaka and Kyoto are increasingly viewed not as peripheral allocations, but as core components of a Japan strategy designed to balance yield, growth and volatility.

Tokyo will always matter. But in today’s Japan, the most compelling opportunities are no longer defined by prestige or scale alone.

For foreign buyers willing to look beyond the capital, secondary cities such as Osaka and Kyoto offer something increasingly rare in global property markets: visible demand, workable pricing and room for active value creation. That combination — rather than headline growth — is quietly reshaping how international capital is flowing into Japan.

Adrian Lim is the senior director and head of international residential sales at Savills Singapore

Adrian Lim is the senior director and head of international residential sales at Savills Singapore

See Also:

AloJapan.com