The Japanese Yen (JPY) is not having the best year-end. A combination of weak economic growth, concerns about government spending, and uncertainty about the Bank of Japan’s (BoJ) monetary policy path has created a perfect storm for the JPY, which has been one of the worst-performing major currencies in the last quarter of 2025.

The USD/JPY pair, however, is set to end the year little changed, opening 2025 near 157.00 and hovering around the 155.00 level by mid-December. In the meantime, a sell-off to levels below 140.00 in April, and episodes of high volatility, which triggered quite serious intervention warnings by Japanese authorities, have made the pair one of the favourites for speculative traders.

The Yen is failing to draw any particular support from the US Dollar’s (USD) weakness, despite the divergence between the US Federal Reserve (Fed) and the BoJ. The Fed is immersed in an easing cycle, and according to the market consensus, it is still far from its terminal rate. The Bank of Japan, on the other hand, hiked interest rates to a 30-year high of 0.75%, in December and hinted at further tightening in the future, but the JPY continued depreciating against its main peers.

Key factors driving the Japanese Yen in 2025: Tariff uncertainty, BoJ monetary and fiscal concerns

The USD/JPY depreciated sharply in the first monts of 2025, but is closing the year on a strong footing after appreciating nearly 10% since May. A confluence of negative factors is looming over the JPY at the moment, but analysing how we reached this point will help us to identify the challenges ahead.

Trump’s tariffs are a highly disruptive element

US President Donald Trump began his second term on January 20 and quickly became a key factor in currency and financial markets. The market shifted its focus to the president’s impulsive and extemporaneous tweets, while most macroeconomic data took a back seat in a revival of the 2017 term, if not worse.

The Republican obtained greater congressional support this time, which encouraged him to take more radical positions than in the first term. As soon as he took office, he announced steep tariffs on basically all US trading partners and started a tit-for-tat trade war with China that kept investors on their toes for weeks.

Trump assured that tariffs would bring trillions in revenue to the US trade balance and would lead to unprecedented employment creation. Market analysts, however, warned that higher import prices would boost consumer inflation and weigh heavily on economic growth.

When the tariff saga was at its height, a raft of negative US macroeconomic figures, namely the 0.3% contraction of the Annualised US Gross Domestic Product (GDP) in the first quarter, finally revised to a 0.5% decline, confirmed the worst fears. The US economy contracted for the first time in three years, which hammered the idea of US exceptionalism amid a global downturn, as the economies of China and the Eurozone showed clear signs of weakening.

Around that period, Trump also started bullying Federal Reserve Chairman Jerome Powell for not lowering interest rates fast enough, replaced Adriana Kluger with Stephen Miran, a dove loyalist, and manoeuvred to oust Governor Lisa Cook on allegations of mortgage fraud. These unprecedented attacks eroded investors’ confidence in the US central bank’s independence and its ability to set monetary policy solely on macroeconomic data.

Against this backdrop, the US Dollar depreciated against its main peers during most of the first half of the year, sending the USD/JPY to test the 2024 lows in the 140.00. After that, the pair rallied relentlessly due to reasons that will be analysed next.

Japanese Yen in 2026: Headwinds likely to remainBoJ’s monetary policy uncertainty will remain a key JPY driver

The Bank of Japan has been a key factor in shaping the Yen’s direction this year and will remain highly relevant in the next one. The BoJ hiked rates by a quarter point in January to its highest level in 17 years, at 0.5%, and upgraded its inflation outlook, which the market took as a sign that further monetary tightening would follow sooner or later.

That provided additional support to the Yen and helped to boost the Japanese currency in the first quarter of the year, but the bank hesitated, stepped back and kept delaying the next interest rate hike. At some point, investors lost their patience, and the Yen started a steady depreciation in the second half of the year.

The BoJ finally raised rates by a further 25 basis points to 0.75% after its December 19 meeting, and Governor Kazuo Ueda showed confidence that wage rises will contribute to keeping inflation steady, hinting at further rate hikes in the future. The market reaction, selling the Yen across the board, reveals that investors remain sceptical.

All things considered, 0.75% is still a relatively low level compared with the rest of the major central banks, and significantly low given that yearly inflation is at 3%. Furthermore, the path forward remains uncertain.

BoJ Governor Ueda said, after December’s meeting, that further rate hikes will depend on economic and inflation forecasts, and remained elusive about the neutral rate. The market consensus points to 1.00% to 1.25%, which means between one and two further rate hikes, but the Japanese Prime Minister Sanae Takaichi is a known supporter of accommodative monetary policies and will, highly likely, oppose a steep monetary tightening cycle.

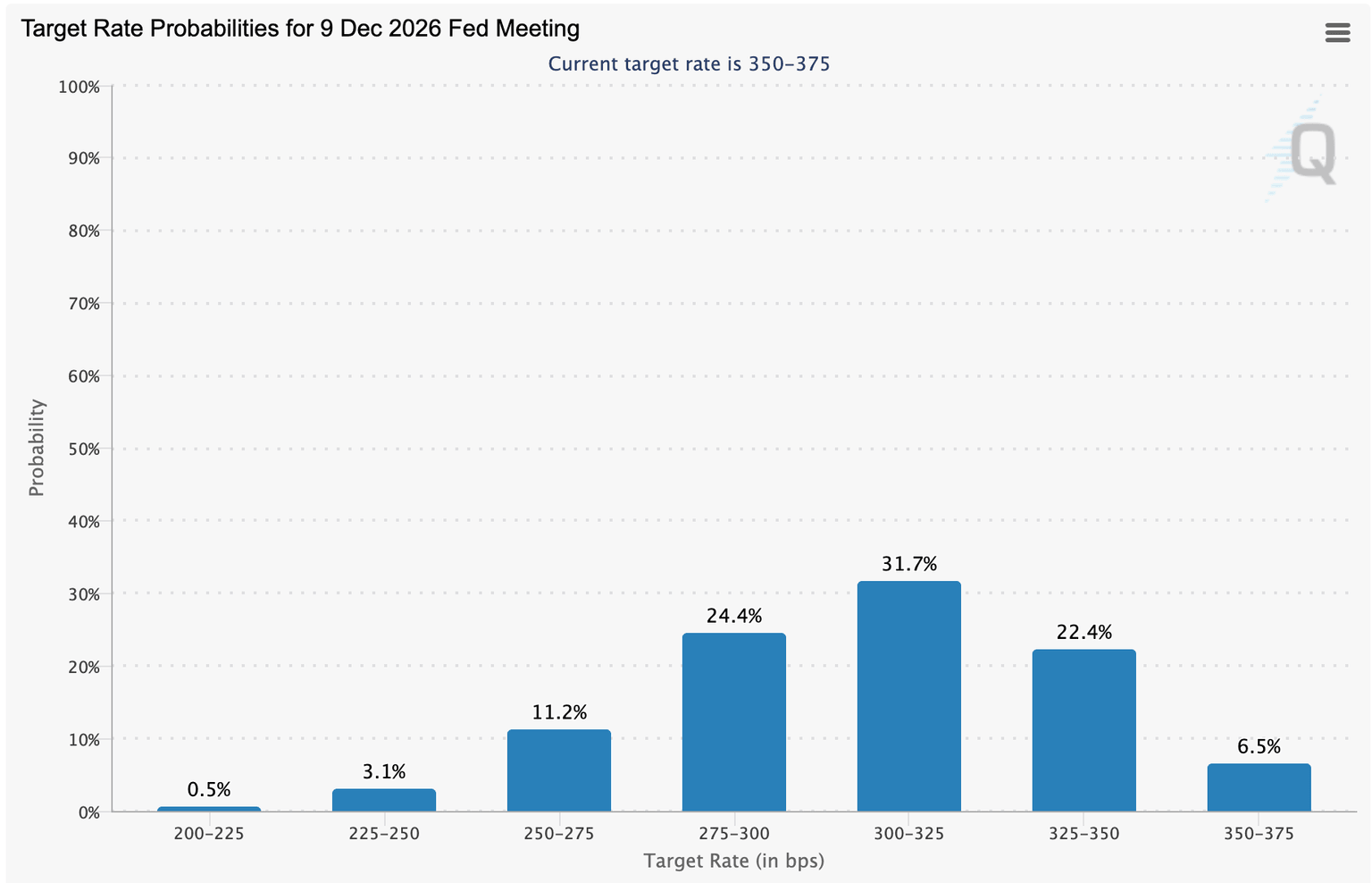

This might keep the Japanese Yen under pressure in 2026, especially if the US Federal Reserve finally meets December’s interest rate projections and delivers only one further rate cut through the year.

PM Takaichi and the risk of a Liz Truss moment

The Yen, which was already trading lower since early April, accelerated its decline in October, when Sanae Takaichi became Japan’s Prime Minister. Takaichi, a former assistant to Prime Minister Shinzo Abe, came with a pledge to revive his mentor’s policies of high public spending and low borrowing costs to boost economic growth.

One of the cabinet’s first decisions was to approve a $137 billion stimulus package to help households cope with rising living costs, which has put investors on edge. Beyond that, recent news reports by Nikkei Business suggest that the cabinet is drawing plans to introduce additional tax exemptions to foster corporate investment.

All these measures will be financed with debt, and are expected to add pressure on the already strained public finances. Japan’s government debt was at 203% of the country’s Gross Domestic Product in the third quarter of 2025, according to data by CEIC.

At the moment of writing, the Japanese Parliament is discussing the approval of a $117 billion supplementary budget to finance Takaichi’s stimulus plan. These measures have raised concerns in bond markets and have sent Japan’s Government bond yields rallying. The yield for the benchmark 10-year note has reached 18-year highs. Recent bond auctions have attracted strong demand, but the risks of a credit crisis are real. If the tide turns, a scenario akin to the one seen in the United Kingdom in October 2022 would send the Yen into a tailspin

A bright Japanese economic outlook would help ease investors’ fears, but so far, it does not seem to be the case. The cabinet office revised the third quarter’s GDP figures down to a 2.3% annualised contraction, from previous estimations of a 1.8% decline. Business investment fell for the first time in the last six quarters, as uncertainty about Trump’s trade tariffs keeps weighing on exporting activity. Beyond that, household spending remains depressed, amid the high consumer prices, while the weak Japanese Yen contributes to spurring inflationary pressures.

The latest economic projections from the Bank of Japan point to only moderate growth in the near term, with exports and production likely to show weakness amid the slowdown in overseas economies, and corporate profits likely to decline. The bank expects the accommodative financial conditions to offset some of these hindrances.

Consumer prices have been rising steadily in the second half of the year, driven by higher food and energy prices. Headline National Price Index (CPI) inflation reached 3% in October before easing to a 2.9% year-on-year rate in November, which has raised concerns that the BoJ’s monetary policy might be behind the curve.

The central bank, however, remains confident that core CPI, which has been growing at a steady 3% yearly rate in October and November, will slow to levels below 2% in the first half of the 2026 fiscal year, to pick up thereafter as economic growth boosts demand for employment and pushes wages higher. The Japanese Yen would need this scenario to crystallise to be able to perform a sustained recovery.

FX intervention risks are far from over

The possibility of an intervention by the Bank of Japan to support the Yen has been present during the second half of the year and is likely to remain a real risk unless USD/JPY retreats from current highs.

Investors’ confidence that the BoJ was set to hike interest rates in December, coupled with rising bets that the Fed will significantly lower borrowing costs in 2026, contributed to eased Yen weakness over the last few weeks. Still, the Japanese Finance Minister, Satsuki Katayama, has warned in recent weeks that some episodes of Yen depreciation do not reflect fundamental factors and that Japanese authorities stand ready to support the currency against speculative movements.

The pair is still relatively far away from the 161.95 high that triggered an alleged intervention in 2024. The BoJ does not confirm or deny monetary interventions, and the Japanese authorities have reminded that they are more concerned about market volatility than about a specific exchange rate.

Nevertheless, the weak Japanese economic outlook and investors’ concerns about the country’s fiscal health are expected to weigh on the Yen. Looking forward, the 160.00 level in the USD/JPY is considered a line in the sand. If the pair surges above that level, Tokyo might be forced to step in.

Fed monetary policy will be the main US Dollar driver

Regarding the US Dollar, the US Federal Reserve cut the Federal Funds Rate by 25 basis points to the 3.50% to 3.75% range in December, and Chairman Jerome Powell hinted at a pause over the coming months. With that in mind, a widely divided Monetary Policy Committee and the tension between the bank’s two mandates, employment and inflation, make it very difficult to anticipate the pace and the depth of the central bank’s easing cycle.

Recent employment data points to a stalled labour market, which adds pressure on the bank to cut interest rates further. Consumer inflation declined unexpectedly in November, but the final figures are likely distorted by the US Government shutdown. Furthermore, US President Trump continues to threaten with higher tariffs on some of the country’s main trading partners. And the trade relations with China remain prone to the odd disagreement, ultimately leading to higher tariffs and increasing import prices.

The latest Fed’s interest rate projections, the so-called “dot plot”, signalled only one further rate cut for 2026. Markets, instead, remain confident that the bank will likely cut rates between two and three times next year. Especially considering that the bank’s Chairman will be replaced in May.

Chair Jerome Powell ends his eighth-year term in 2026, and President Trump is likely to announce his replacement in the coming weeks. The best positioned for the job are the former Fed governor, Kevin Warsh, and the director of the National Economic Council, Kevin Hassett. Trump has also mentioned Governor Christopher Waller. Anyway, the disposition to drastically reduce borrowing costs constitutes a sine qua non for the next Fed chief.

The nomination is likely to come in the next weeks and will probably be taken by the market as confirmation of the bank’s commitment to a more accommodative monetary policy. In FX markets, this is likely to increase the US Dollar’s weakness and provide additional support for the Japanese Yen. A significant Yen recovery, however, looks improbable unless the BoJ shows a clear commitment to keep tightening its monetary policy, supported by evident signs of an economic improvement.

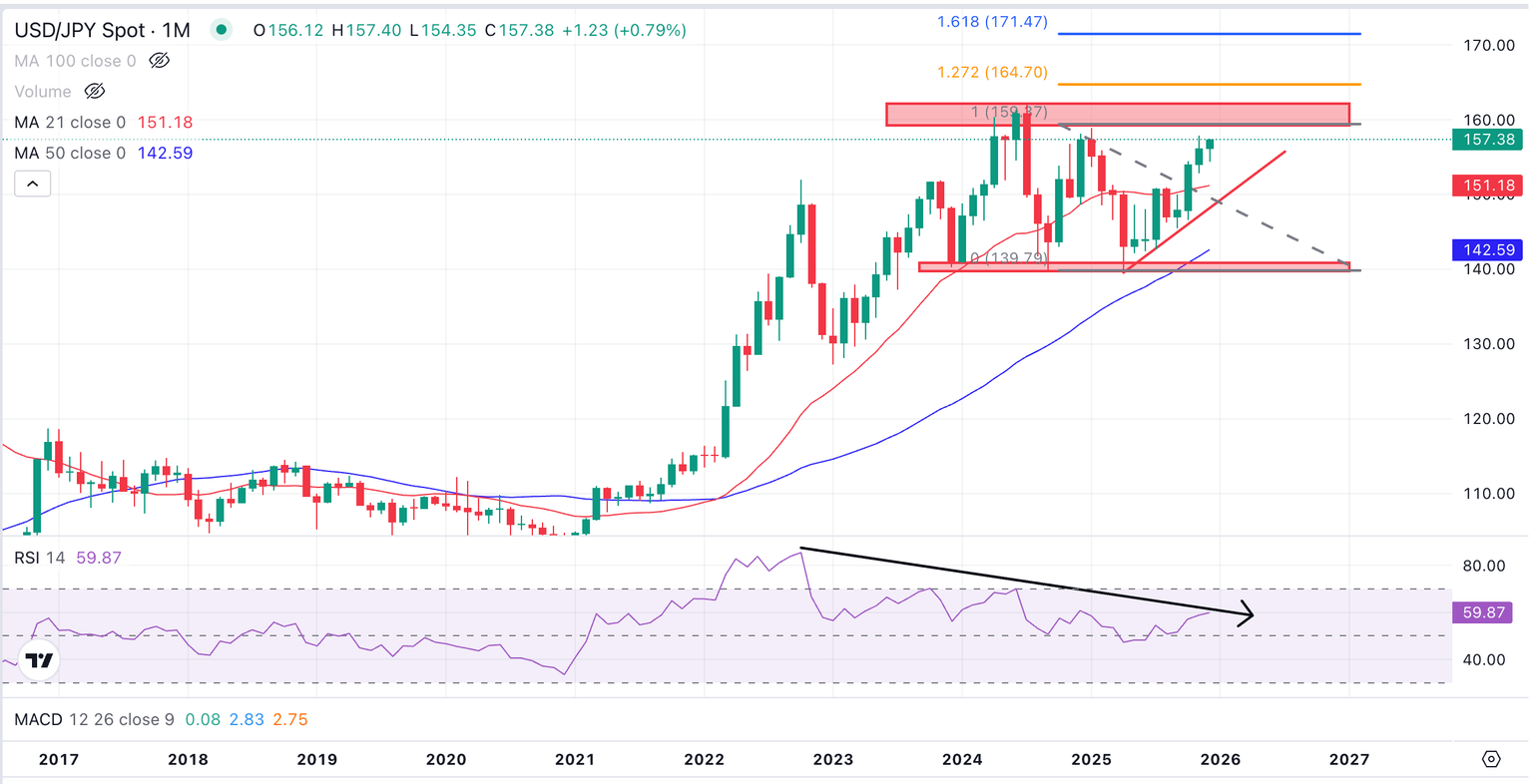

USD/JPY Technical Outlook: In a bullish trend, near the 160.00 level

A look at the monthly chart shows a firm USD/JPY pair, trading right below the yearly high. The US Dollar has appreciated against the Japanese Yen in six of the last seven months, and rallied nearly 6% between October and November, highlighting a clear bullish trend.

The 50-period Simple Moving Average (SMA) is showing a strong upward slope, and the monthly Relative Strength Index (RSI) is in bullish territory but still far from overbought levels. A bearish divergence and the strong resistance above 160.00 are a warning sign, though the pair is not yet hinting at a trend shift.

Bulls remain focused on the area between the yearly high at 157.89 and the 2024 high at 161.95, which is likely to be a tough one. Further up, the 127.2% Fibonacci extension of the January-April sell-off, at 164.70 and the 170.00 psychological level, emerges as the following bullish targets.

Downside attempts would have to extend below the 21-month SMA, in the area of the 151.00 level, and a trendline from early April lows, now around 149.00. A confirmation below those levels might give bears the confidence to test the 50-month SMA, in the vicinity of 142.50, before heading to the key support area around 140.00.

Conclusion

All in all, the Yen is on the back foot in December, unable to make any significant advance amid the generalised US Dollar weakness and the monetary divergence between the Fed and the Bank of Japan, and is likely to remain that way unless the context changes drastically in 2026.

The cautious stance of the Bank of Japan is one of the main reasons to keep the Yen from appreciating further. The bank hiked rates in December, but conditioned further rate hikes on the evolution of the economic and inflationary trends. The Japanese government has tolerated this hike, but might not be happy about a steep monetary-tightening cycle.

Japan’s cabinet has approved a stimulus plan that has brought concerns about the country’s fiscal stability to the fore. In this context, markets will be especially sensitive about signals of further economic deterioration in Japan. The risk of a credit crisis is real.

Finally, a dovish Fed might launch a lifeline to the Yen. The US central bank anticipates only 25-basis-point rate cuts in 2026, but the market remains confident that there will be more. Expectations that a more dovish candidate will replace Chairman Powell are endorsing those views. This has given some oxygen to an ailing Yen and might allow for further Yen recovery once the name of the next Fed chief is confirmed.

AloJapan.com