After Shares Rise 26%")

Osaka Organic Chemical Industry Ltd. (TSE:4187) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 34%.

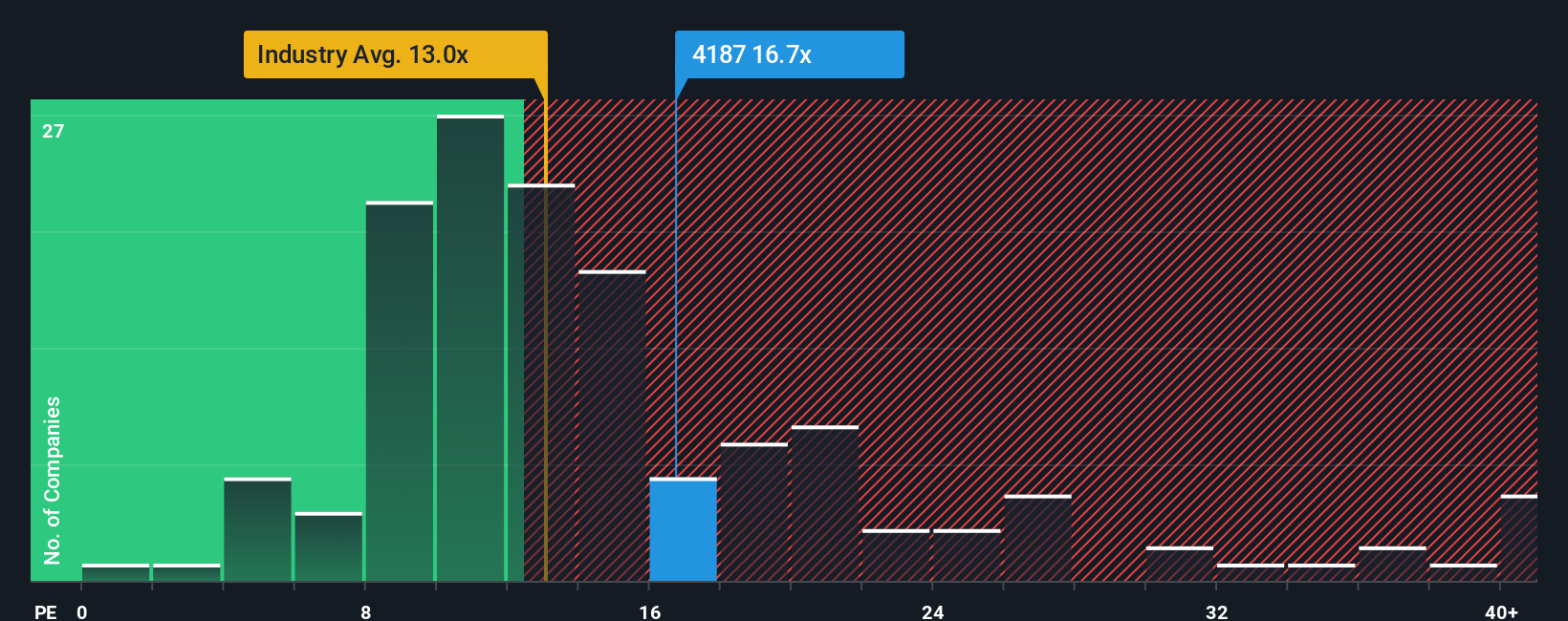

After such a large jump in price, Osaka Organic Chemical Industry may be sending bearish signals at the moment with its price-to-earnings (or “P/E”) ratio of 16.7x, since almost half of all companies in Japan have P/E ratios under 14x and even P/E’s lower than 10x are not unusual. Nonetheless, we’d need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

Osaka Organic Chemical Industry certainly has been doing a good job lately as it’s been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You’d really hope so, otherwise you’re paying a pretty hefty price for no particular reason.

See our latest analysis for Osaka Organic Chemical Industry

TSE:4187 Price to Earnings Ratio vs Industry October 31st 2025 If you’d like to see what analysts are forecasting going forward, you should check out our free report on Osaka Organic Chemical Industry. Is There Enough Growth For Osaka Organic Chemical Industry?

TSE:4187 Price to Earnings Ratio vs Industry October 31st 2025 If you’d like to see what analysts are forecasting going forward, you should check out our free report on Osaka Organic Chemical Industry. Is There Enough Growth For Osaka Organic Chemical Industry?

There’s an inherent assumption that a company should outperform the market for P/E ratios like Osaka Organic Chemical Industry’s to be considered reasonable.

Retrospectively, the last year delivered an exceptional 41% gain to the company’s bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Therefore, it’s fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 3.9% during the coming year according to the six analysts following the company. With the market predicted to deliver 11% growth , the company is positioned for a weaker earnings result.

In light of this, it’s alarming that Osaka Organic Chemical Industry’s P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company’s business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Osaka Organic Chemical Industry’s P/E

Osaka Organic Chemical Industry shares have received a push in the right direction, but its P/E is elevated too. We’d say the price-to-earnings ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Osaka Organic Chemical Industry’s analyst forecasts revealed that its inferior earnings outlook isn’t impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it’s very challenging to accept these prices as being reasonable.

You should always think about risks. Case in point, we’ve spotted 1 warning sign for Osaka Organic Chemical Industry you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

AloJapan.com