Investment Narrative?")

Recent analysis highlights JAPAN MATERIAL’s role as a critical supplier in the semiconductor industry, with the company set to gain from expected collaborations with Rapidus and TSMC’s Kumamoto plant. This positions JAPAN MATERIAL to potentially capture new opportunities as semiconductor supply chains expand to meet growing global demand. Let’s explore how JAPAN MATERIAL’s involvement with major semiconductor projects shapes its investment narrative and future growth prospects.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump’s tariffs. Discover why before your portfolio feels the trade war pinch.

What Is JAPAN MATERIAL’s Investment Narrative?

For anyone considering JAPAN MATERIAL today, the investment story hinges on the company’s role as a crucial partner in the semiconductor supply chain. The recent news of collaborations with Rapidus and TSMC’s Kumamoto plant highlights a real, and possibly significant, catalyst that could accelerate growth prospects beyond what earlier analysis captured. Before this news, forecasts pointed to solid but not extraordinary annual growth, and valuation concerns lingered, with shares seen as expensive versus industry averages and a slight premium to consensus fair value. Short-term catalysts were largely tied to regular earnings cycles, margin improvements, and dividend increases, but this new supply chain involvement could shift attention to capacity, contract wins, or new customer announcements as the next big drivers. At the same time, risks around high valuation, recent share price volatility, and a profit outlook tied closely to the industry cycle are still important considerations.

However, a sharp shift in chip industry orders could reshape this outlook quickly.

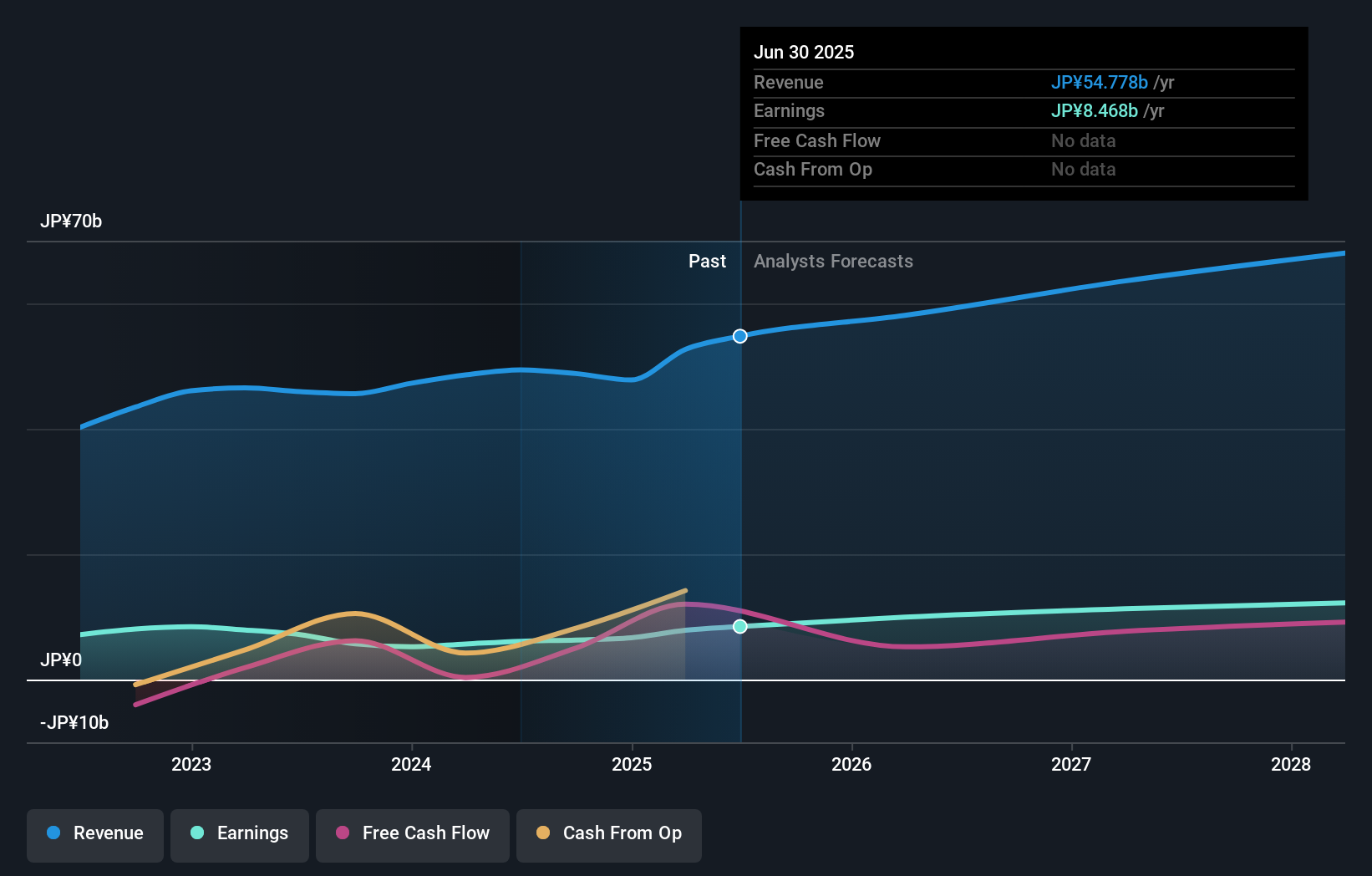

JAPAN MATERIAL’s share price has been on the slide but might be up to 10% below fair value. Find out if it’s a bargain.Exploring Other Perspectives TSE:6055 Earnings & Revenue Growth as at Oct 2025 Investor fair value estimates from the Simply Wall St Community currently cluster at ¥2,200, reflecting a uniform view here. With only one perspective included, contrast this with the shifting catalysts and risks after JAPAN MATERIAL’s latest news, and you’ll see why opinions could change quickly. Consider reviewing alternative viewpoints for a wider picture.

TSE:6055 Earnings & Revenue Growth as at Oct 2025 Investor fair value estimates from the Simply Wall St Community currently cluster at ¥2,200, reflecting a uniform view here. With only one perspective included, contrast this with the shifting catalysts and risks after JAPAN MATERIAL’s latest news, and you’ll see why opinions could change quickly. Consider reviewing alternative viewpoints for a wider picture.

Explore another fair value estimate on JAPAN MATERIAL – why the stock might be worth just ¥2200!

Build Your Own JAPAN MATERIAL Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

No Opportunity In JAPAN MATERIAL?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

AloJapan.com