Advertisers face sustained, embedded media inflation, with the new 4% global trendline signalling that the global media economy has settled into a new normal of moderate but persistent inflation, mirroring the wider economy.

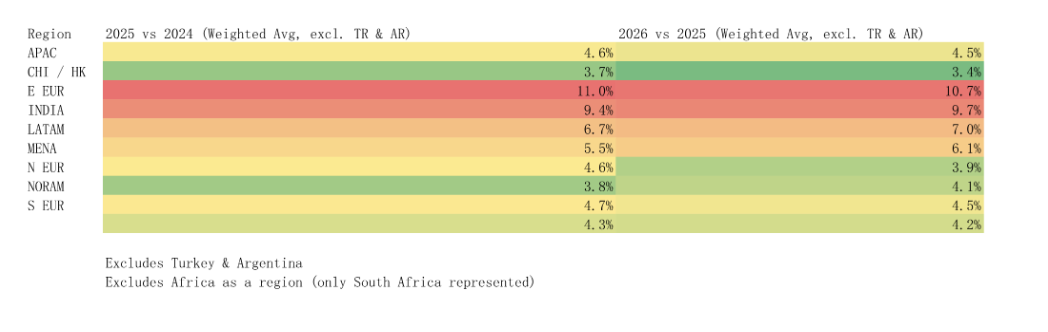

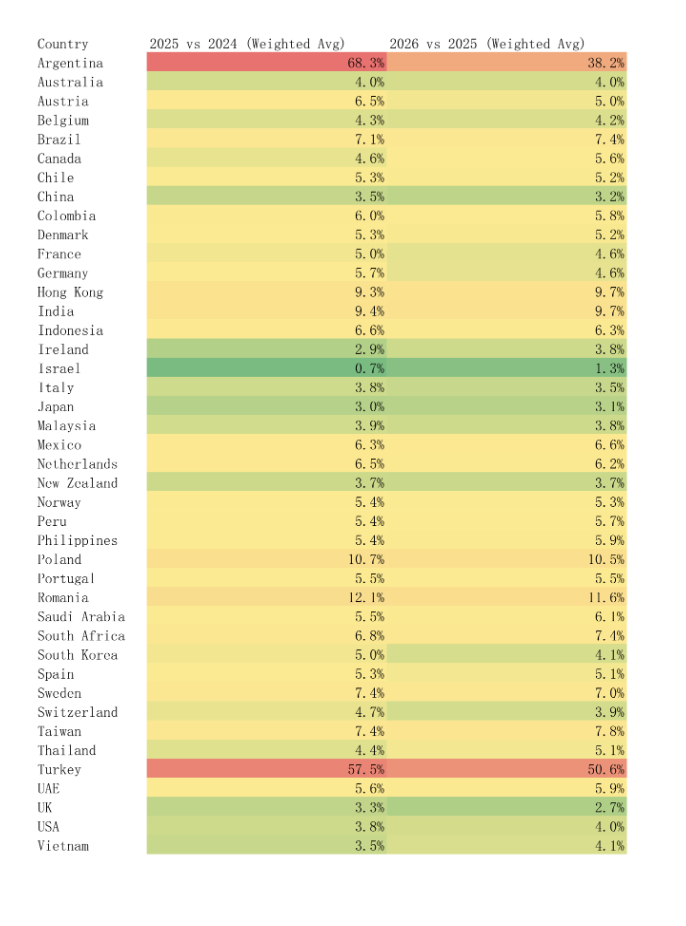

Across APAC media inflation is moderating around 4.6% for the region (4.55% in 2025 and 4.46% in 2026). APAC shows two different stories: inflation is steady in Japan (around 3%) but accelerating strongly in India and Hong Kong, with India seeing the steepest price growth in APAC (about 9.4%), and Hong Kong closely behind (about 9.3%), while in Taiwan its seen at (7.4%–7.8%) and Thailand (4.4%–5.1%). Inflation here is driven less by supply scarcity and more by rising audience value and domestic advertiser demand.

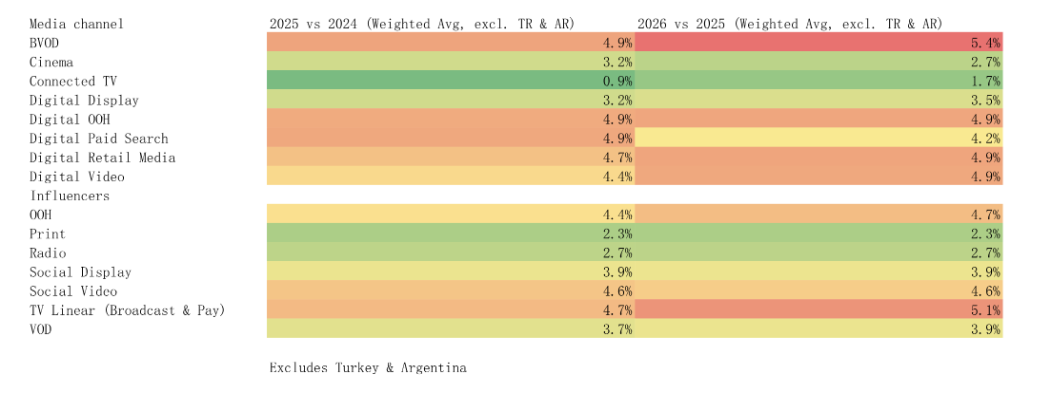

Video remains king, but not all screens are equal

While broadcaster video-on-demand (BVOD) commands the strongest price inflation of any channel (around +5% per year), prices for Connected TV (CTV) are almost flat (1%). WFA Outlook contributors say supply is still running ahead of demand, and even in the US, the most mature market, price increases are moderate.

By region, BVOD in APAC sees price inflation stand at 4.2% for 2025 vs 2024, and 5.1% 2026 vs 2025. India sees one of the highest price inflations for BVOD (10.3%) and for connected TV (12.6%).

Buyers continue to pay a premium for trusted, curated broadcaster environments that balance reach with measurement confidence, while CTV’s fragmented, programmatic supply is dampening its pricing power.

Other channels in APAC such as Cinema, Digital Display, Digital OOH, and Print show generally lower inflation rates (2%–4%), reflecting different market dynamics.

Linear TV inflation remains around 5%, though in many countries this is explained by steadily eroding viewing, particularly of audiences which are scarcer and thus in higher demand.

Global contrasts

Beyond APAC’s moderate 4.6%, inflation is notably higher in Eastern Europe (11%) and Latin America (6.7%), while mature Western economies show moderation around 3-4%. For example, the US is forecast to experience media inflation of about 3.8% in 2025, rising slightly to around 4.0% in 2026. The UK sees slightly lower inflation but rising prices signal caution.

“Embedded media price inflation requires advertisers to constantly find new ways to make their ad budgets work harder,” says Tom Ashby, global lead, media services at WFA. “By understanding how prices are moving by market, by region and by channel, WFA members can make more informed media investment choices, reaching their target audience more efficiently and therefore drive better campaign effectiveness.”

AloJapan.com