After Shares Rise 33%")

JAPAN MATERIAL Co., Ltd. (TSE:6055) shareholders have had their patience rewarded with a 33% share price jump in the last month. Unfortunately, despite the strong performance over the last month, the full year gain of 2.8% isn’t as attractive.

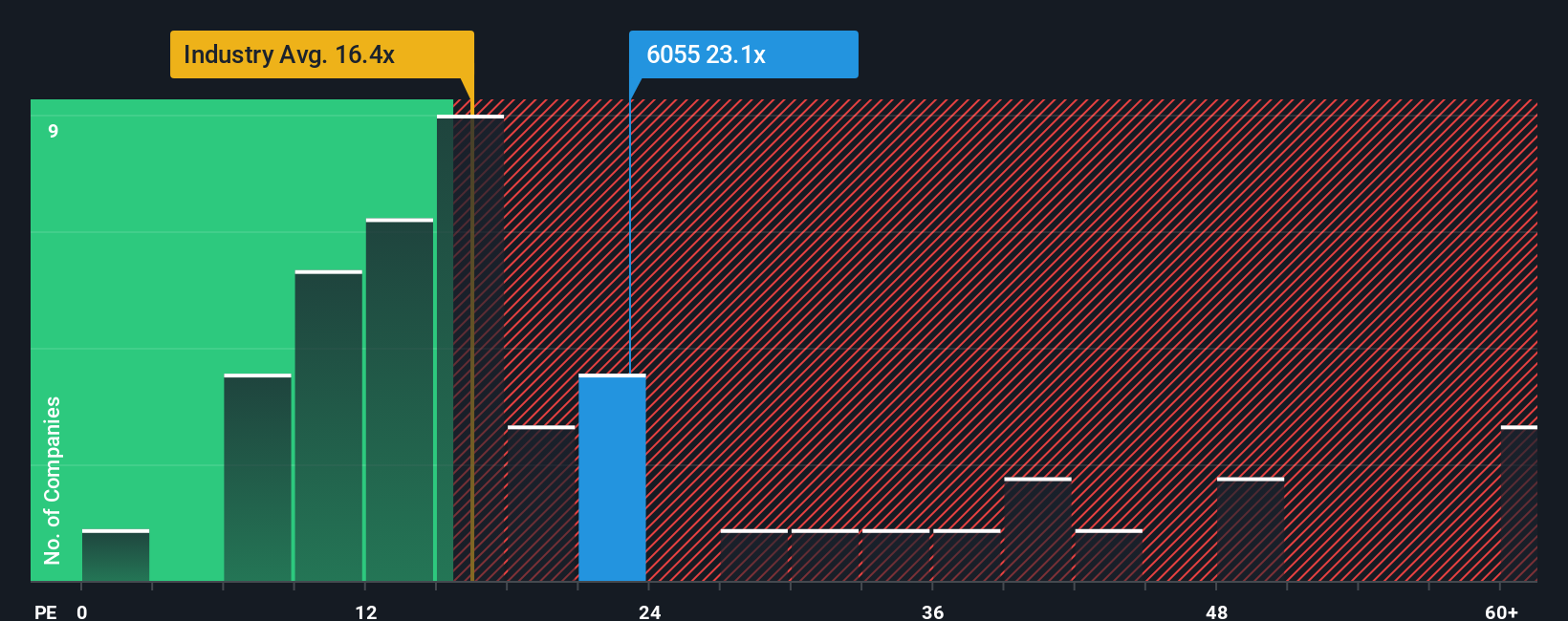

Since its price has surged higher, given close to half the companies in Japan have price-to-earnings ratios (or “P/E’s”) below 14x, you may consider JAPAN MATERIAL as a stock to avoid entirely with its 23.1x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it’s justified.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10bn in marketcap – there is still time to get in early.

With earnings growth that’s superior to most other companies of late, JAPAN MATERIAL has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You’d really hope so, otherwise you’re paying a pretty hefty price for no particular reason.

See our latest analysis for JAPAN MATERIAL

TSE:6055 Price to Earnings Ratio vs Industry September 19th 2025 If you’d like to see what analysts are forecasting going forward, you should check out our free report on JAPAN MATERIAL. Is There Enough Growth For JAPAN MATERIAL?

TSE:6055 Price to Earnings Ratio vs Industry September 19th 2025 If you’d like to see what analysts are forecasting going forward, you should check out our free report on JAPAN MATERIAL. Is There Enough Growth For JAPAN MATERIAL?

In order to justify its P/E ratio, JAPAN MATERIAL would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 39%. As a result, it also grew EPS by 18% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 11% per annum during the coming three years according to the five analysts following the company. Meanwhile, the rest of the market is forecast to expand by 9.6% each year, which is not materially different.

With this information, we find it interesting that JAPAN MATERIAL is trading at a high P/E compared to the market. Apparently many investors in the company are more bullish than analysts indicate and aren’t willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

What We Can Learn From JAPAN MATERIAL’s P/E?

The strong share price surge has got JAPAN MATERIAL’s P/E rushing to great heights as well. Typically, we’d caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We’ve established that JAPAN MATERIAL currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve, it’s challenging to accept these prices as being reasonable.

Having said that, be aware JAPAN MATERIAL is showing 1 warning sign in our investment analysis, you should know about.

Of course, you might also be able to find a better stock than JAPAN MATERIAL. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

AloJapan.com